Home » Commentary » Opinion » Interactive Snapshot – Exposing the stealth tax: the bracket creep rip-off

SCROLL DOWN TO ACTIVATE THE GRAPHS

Robert Carling and Michael Potter

– According to CIS modelling, taxpayers in the income decile of $37,500 to $46,500 will be paying an extra $1,300 per year in tax due to bracket creep. Their take home pay will be 3.3% lower than if the bracket creep were fixed.

– The greatest impact is estimated to be on a person earning around $37,100 in today’s money, and the smallest impact is on a person earning around $154,200.

The interactive graph below shows how much you are expected to lose during 2018-19 due to bracket creep. This is the reduction in your yearly take home pay, or equivalently the increase in tax you will pay in 2018-19. The average loss per taxpayer is about $1,180.

The amount you are expected to lose per week is shown in the interactive graph below. The average loss is about $23 per week.

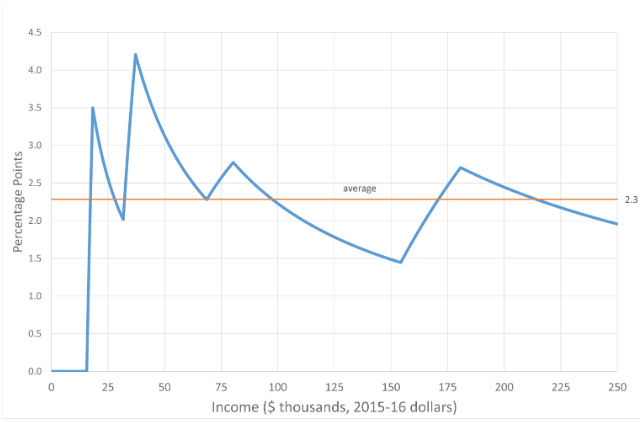

The dollar cost of bracket creep grows with income, as shown in the graphs above. However, the relative impact is different, as shown in the interactive graph below. This shows the percentage point increase in average tax rates due to bracket creep. The average increase is about 2.3 percentage points. In general, the increase in tax rate is greater at low incomes. As a result, bracket creep is broadly regressive, because it hits low income earners harder.

Tax as a share of pre-tax income (or the average tax rate) is increasing year-by-year. The last time there were any income tax cuts was 2012–13. By 2018–19, the average tax rate across all taxpayers will have risen by 2.3 percentage points since 2012–13. The average tax increase will be $1,180 per year or $23 per week. In fact, there has been even more bracket creep, because for all but the lowest tax bracket there has been no threshold adjustment since at least 2010. The figure to the right also shows that bracket creep is affecting all taxpayers, even if they don’t move tax brackets.

Another way of looking at the impact of bracket creep is to calculate the effect on after-tax (take-home) pay.

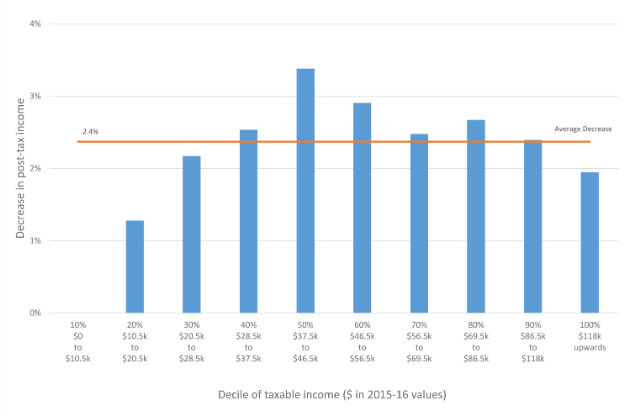

Using 2012–13 as the base year, by 2018–19 take-home pay will be reduced on average by 2.4% because of bracket creep (or $23 per week).

While taxpayers will probably still have higher after-tax income than today, it will be lower than it would be without the impact of bracket creep.

Bracket creep works in a broadly regressive way. The increase in the tax burden and erosion of take-home pay is largest at the lower levels of pre-tax pay. As the figure above (Figure 1 of the main report) shows, the largest percentage reduction in take-home pay is in the $37,500 to $46,500 income range. On average, taxpayers in this range will find their take-home pay 3.3% (or $25 per week) lower than it otherwise would be in 2018–19.

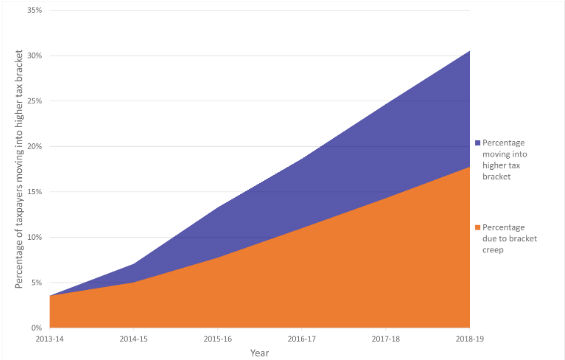

As noted above, all taxpayers are affected by bracket creep, even if they don’t move into higher marginal tax brackets: all taxpayers experience an increase in their average tax rate regardless of their marginal tax rate. However, the economic harm of bracket creep is greater when more people are pushed into higher rate brackets. Over the six years to 2018–19, 4.3 million taxpayers (31% of the total) will move into higher tax brackets, with more than half of those moves due to bracket creep (see figure to right). This particularly exacerbates the disincentives for work in low income households. At higher income levels, this creates incentives for tax minimisation and emigration and discourages innovation, education and investment by unincorporated businesses.

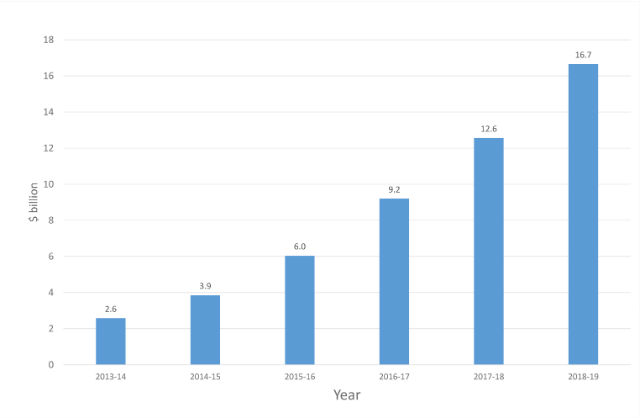

The government’s failure to adjust tax scales since 2012–13 is already reaping an extra $6 billion in revenue this year. By 2018–19, that figure will grow to $16.7 billion in that financial year alone (or a cumulative $51 billion since 2012–13). This is shown in the figure to the left. While this is contributing to budget repair, there are much less economically harmful and more transparent ways to reduce the budget deficit, including stronger expenditure restraint. In fact, bracket creep weakens budget discipline.

Robert Carling is a Senior Fellow at the Centre for Independent Studies. Robert is researching and writing about fiscal policy, taxation and federalism. In addition to working on TARGET30 papers Robert has recently written reports called Shrink Taxation by Shrinking Government! and States of Debt. Prior to joining the CIS, Robert was Executive Director, Economic and Fiscal at the New South Wales Treasury from 1998 to 2006. Previous position have been with Commonwealth Treasury, the World Bank and the International Monetary Fund.

Michael Potter is a Research Fellow at the Centre for Independent Studies. Michael has worked for the Parliamentary Budget Office, the Federal Departments of Treasury, Environment and Prime Minister & Cabinet (where he advised then Prime Minister John Howard on the introduction of the GST). He has also worked as Policy Manager, Economics at the National Farmers’ Federation, and Director, Economics and Taxation at the Australian Chamber of Commerce and Industry.

Research Report 8 (RR8) • ISSN: 2204-8979 (Printed) 2204-9215 (Online) • ISBN: 978-1-922184-57-3 • Published December 2015

Interactive Snapshot – Exposing the stealth tax: the bracket creep rip-off