Introduction

Australia’s natural gas sector has transformed dramatically between 1975 and 2025. What began as a series of isolated gas fields serving local markets evolved into a major export industry that by 2020 temporarily made Australia the world’s largest liquefied natural gas (LNG) exporter. This expansion was overwhelmingly driven by private enterprise — companies prospected new gas basins, invested in massive infrastructure, and created domestic and international markets for Australian gas. Governments, for their part, often reacted to these private-led developments with interventions aimed at securing public interests like supply reliability, affordable prices, and environmental protection.

Yet many of these policies — from domestic gas reservations and price caps to fracking bans — added costs, delays, or uncertainties that reshaped industry decisions. The result is a gas sector moulded by a push-pull dynamic: private developers forging ahead with projects and governments responding under political pressures. They have also resulted in Australia being overtaken by the United States and Qatar on the exports leaderboard.

Australia’s natural gas sector is at a critical juncture. Mounting government intervention — particularly in the last two decades — has stalled investment, restricted exploration, and delayed major projects. These interventions were often politically motivated and poorly aligned with commercial and energy system realities. The results of this are increased costs and risks for the Australian economy.

We need to lift state-based bans and moratoria on onshore gas exploration and unconventional extraction methods such as coal seam gas (CSG) and fracking. These restrictions have constrained new supply and discouraged investment. In addition, approval processes — particularly environmental assessments — should be streamlined to reduce delays and costs, while maintaining appropriate safeguards. Fast-tracking stalled projects, including those in Narrabri and Beetaloo, is essential to preventing forecast supply shortfalls.

Another proposal is to introduce a stable domestic gas reservation policy, similar to the approach used in Western Australia, to ensure a portion of new production is set aside for local use. This could provide price stability for Australian industry while maintaining export opportunities. More broadly, long-term policy certainty is needed to attract investment, which means avoiding ad hoc interventions such as sudden price caps or export restrictions. Policymakers are also urged to adopt a more proactive, strategic approach — such as establishing storage reserves, expanding pipelines, and planning new infrastructure — rather than reacting to crises. Recognising gas as a necessary transition fuel, and ensuring market settings encourage competitive investment, are vital to maintaining reliable energy supply alongside the growth of renewables.

Australia risks ‘too little, too late’ on gas supply. Unless exploration and development are revived, and policy is reset to reflect long-term energy and economic needs, the country could face a dual crisis: escalating energy costs and inadequate firming for the renewables transition. This paper outlines the economic scale of the problem, the policy decisions that created it, and the commercial pathways to recovery.

How much gas do we really have?

Natural gas evolved in several forms. Initially it was associated with oil production and was essentially a waste product. When markets were developed it was supplemented with gas fields that were developed in their own right. All of this was known as conventional gas after alternatives were sourced with new technology largely based on coal seam methane. Later more sources were discovered by fracturing shale.

In 2022, Australia’s ‘proven and probable’ (2P) reserves for conventional gas were estimated at a considerable 78,061 petajoules (PJ), which is about 69.41 trillion cubic feet (Tcf). For ‘identified resources’ (which include contingent resources) the 2022 figures for conventional gas are about 98,649 PJ (~87.71 Tcf). For coal-seam gas (CSG) in 2022 the 2P reserves were estimated at 30,859 PJ (~27.44 Tcf). A large portion of these reside in Queensland in the Bowen and Surat basins; (i.e., a major share of its ‘untapped’ resource base).[1] ‘Untapped’ typically refers to reserves that are 2P but not yet developed (or under construction) — resources with potential for future production but requiring new investment or infrastructure. Regulatory, environmental, and infrastructure hurdles can convert ‘reserves’ into ‘resources that remain undeveloped’. So ‘untapped’ is not the same as ‘immediately producible’.[2]

The vast majority (~93 %) of the conventional gas resources are located off the north-west coast of Western Australia in the North West Shelf region: Northern Carnarvon, Browse, Bonaparte basins. Onshore, the greatest quantity of identified remaining CSG resources lies in Queensland’s Bowen & Surat basins.

The Queensland government’s own Gas Industry Overview outlines that the state alone holds “more than 29,000 PJ of proven and probable gas reserves” (inclusive of CSG and conventional) and that these reserves are sufficient to meet demand for more than two decades.[3] Queensland has large reserves of CSG and relatively small conventional gas reserves.[4]

Some estimates reflect reserves that are ‘discovered’ and reported (2P or similar), but do not necessarily reflect extractable volumes under current economic, regulatory or infrastructure conditions. So, for example, while Queensland may have 29,000 PJ+ in reserve, for example, not all of that is necessarily ready for production tomorrow.

Why gas exploration bans were implemented

The principal reason most Australian state governments banned or imposed moratoria on onshore gas exploration is a response to environmental and community concerns.

In Victoria, for example, the permanent ban on unconventional gas extraction (including fracking and CSG) was fuelled by fears it could threaten groundwater and agricultural land, and concerns that chemicals or saltwater might contaminate water tables and farmlands.[5] Strong community resistance, especially from farming and rural regions, played a pivotal role. Campaigns such as those in Victoria framed onshore gas as a threat to local agriculture, environmental health, and rural values. Broader issues such as climate impact, CO₂ emissions, and potential health effects from gas extraction methods further reinforced political will to restrict exploration.[6]

These concerns became enshrined in law. Victoria introduced the Resources Legislation Amendment (Fracking Ban) Act 2017, permanently banning unconventional gas. This was later strengthened when the ban was constitutionally enshrined.[7] However, the above concerns were largely generated by activists who wanted to eliminate fossil fuels. The Victorian government in the main drove these claims with legislation without regard for the consequences of energy shortages.

Costs and risks

The problem is now plain: a looming supply crunch, surging energy prices, industrial contraction, and heightened energy security risks. Despite abundant gas reserves, government-imposed moratoria, price caps, and regulatory uncertainty have constrained domestic development, especially on the east coast. The reserve-to-production ratio in key regions has collapsed from decade-earlier levels (exploration expenditure down by roughly three-quarters over the last decade) and onshore exploration activity in some states (eg. Victoria) fell to almost zero during moratorium years, effectively a near-100% drop in onshore drilling.[8] [9] This situation has imposed significant costs — with heavy industries being closed or subsidised to survive — and brings serious risks.

Supply risks

Supply-side constraints are largely self-inflicted. Although Australia has become one of the world’s largest LNG exporters, oil and gas exploration has dropped sharply over the past two decades. Offshore exploration has been hit hardest: the number of new wells drilled has plunged from more than 50 in 2010 to just 3 in 2023.[10] This decline in new discoveries will have serious consequences for the future supply pipeline, affecting both the quality of projects and their ability to sustain LNG and domestic gas facilities.

State bans and uncertainty over approvals have deterred explorers, and it shows — petroleum exploration activity has stalled in Australia. This precipitous decline in drilling has occurred even as eastern Australia’s gas demand (for industry, households, and power generation) remained substantial. Industry data indicate eastern 2P gas reserves are not being replaced at the rate of consumption. Meanwhile, existing fields in traditional basins (e.g. Gippsland in Victoria) are in decline,[11] and replacements like NSW’s Narrabri project have been mired in delays (Narrabri gas field was approved in 2020 but as of 2025 has delivered no gas). In short, moratoria and protracted approvals have choked off exploration and new development, directly contributing to today’s tight supply. The consequence has been a heavier reliance on interstate gas and costly LNG imports to make up the shortfall.

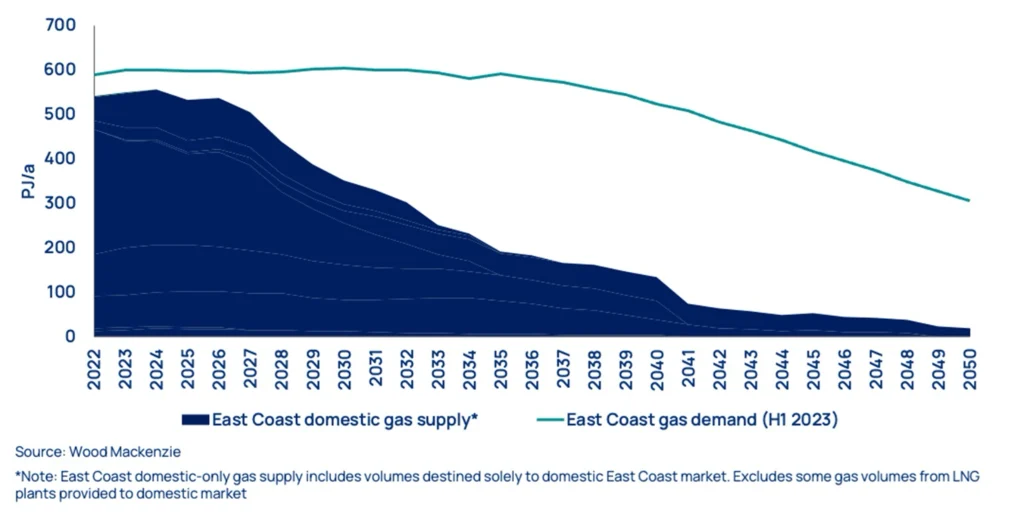

And as legacy gas fields in the Gippsland, Otway, and Cooper basins decline, NSW and Victoria face structural supply gaps from 2027–28 onward unless major new developments (e.g. Narrabri, Beetaloo) proceed.[12]

Fig 1: Projected East Coast Gas Demand vs Supply (2022-2050)

AEMO projects shortfalls from 2027, saying Victoria, which has the large Bass Strait reserves, will run short of gas in 2028 and “forecasts a gap in gas supply for southern states from 2028 due to declining Bass Strait production”.[13] Further, Frontier Economics models a 15% supply deficit by 2030 under current policy. The Australian Pipelines and Gas Association (APGA) cites the “bleakest short‑term gas supply outlook ever modelled by AEMO”. APGA warns that without new structural supply, there is risk of “economic destruction of the more than A$250 billion of enabled commercial activity” across NSW, QLD and Victoria alone, which is at risk if gas shortages and high prices persist.[14] The Australian Competition and Consumer Commission (ACCC) predicts gas shortfalls for all the eastern states from late 2025 into 2026–2028 if all un-contracted Queensland LNG is exported, creating downstream risks for industries across these states.[15] Queensland is a net supply source, but much of its production is committed to exports, limiting buffer capacity for eastern states when they need it most.

Tasmania uses very low levels of natural gas, primarily for residential heating and small-scale commercial uses, so industry exposure is small compared to mainland states. However, coal-powered industries in the state that want to electrify are being told there is already insufficient electricity supply.[16] The Boyer Paper Mill, located on the Derwent River near Hobart, planned to replace coal-fired boilers with electric boilers, aiming to reduce emissions and future-proof operations. However, Hydro Tasmania has stated that Tasmania’s grid lacks the capacity to supply the additional 45 megawatts needed. The mill currently consumes around 100 MW; the transition would require nearly half again more. Hydro Tasmania said its only alternatives are activating gas-fired backup generation or importing electricity from Victoria — both costly options. The mill was reportedly offered power via imports at much higher prices.[17]

Further, southern states rely on gas‑fired generators to firm the grid, especially during winter peaks when renewables underperform. Shortfalls can force generators to switch to more costly diesel backup, elevating wholesale electricity prices.[18]

Economic consequences

Decisions to constrain gas development carry quantifiable economic costs. Costs of gas to manufacturing industries have tripled since 2015,[19] while household gas prices have increased 34% over the past three years, with even larger rises in New South Wales (38%) and South Australia (36%).[20]

In New South Wales alone, gas-intensive manufacturing sectors (such as chemicals and fertilisers) contribute roughly $2.3 billion in annual output[21] — economic activity put at risk if gas supply falters. According to Dr Alex Robson, a permanent 10% increase in domestic gas prices is estimated to cause a ~0.19% reduction in GDP, equivalent to around $3.5 billion annually. NSW Treasury has estimated that each year of delay imposes around $450 million in deadweight economic loss.[22] A combined 10% increase in both gas and electricity prices could shrink GDP by ~0.46% (~$8.5 billion) each year.[23]

Today the east coast’s reserve-to-production (R/P) ratio is alarmingly low — proven and probable (2P) reserves would cover only about 17 years of demand[24] at current usage. By contrast, Western Australia’s domestic gas reservation has helped maintain a far healthier R/P buffer. The bottom line is that underinvestment and project delays have real costs: lost GDP from forgone industrial output, higher energy expenses for families and businesses, and diminished energy security.

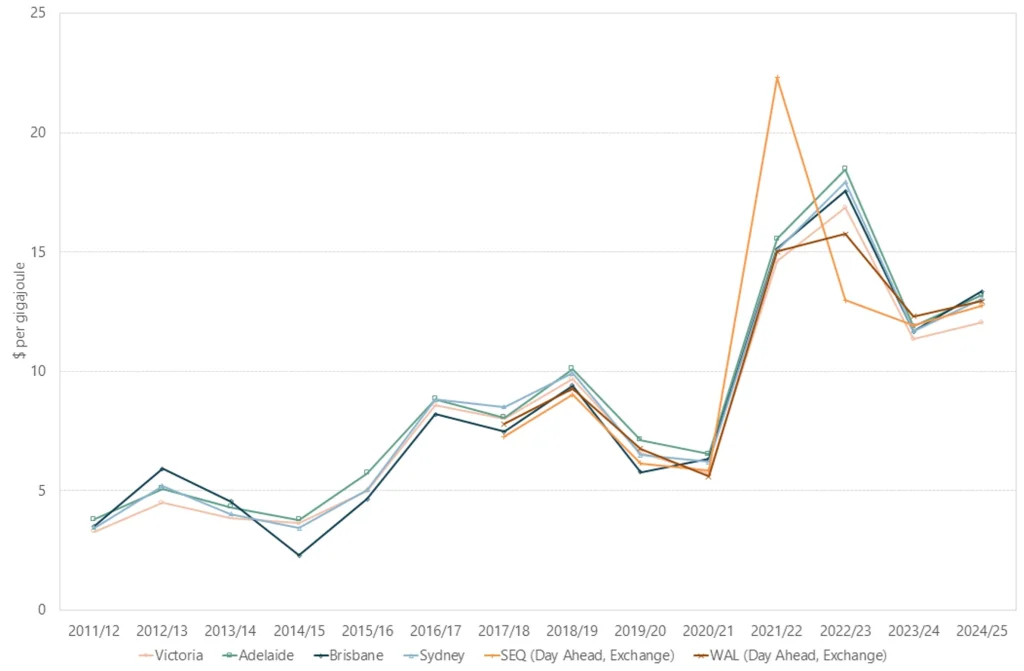

Fig 2: Australian gas market prices 2011-2025

Source: Australian Energy Regulator[25]

Impacts on industry

Australia’s energy-intensive industries — including aluminium, chemicals, food and beverage, and paper — have been among the first to feel the squeeze from gas un-affordability, with several case studies highlighting financial strain during price spikes. For example, Melbourne-based bakery Heather Brae Shortbreads reported annual energy bills jumping to $300,000 due to rising gas costs, threatening viability.[26] Chemical and petrochemical industries also rely on gas as a chemical feedstock and energy source. Even moderate gas supply disruption or price hikes can dramatically impact production viability and exports.[27]

A stark example is the Tomago aluminium smelter in NSW — the country’s largest single electricity user — which on multiple occasions was forced to curtail or temporarily shut down operations due to energy price spikes. In May 2021, Tomago “stopped running three times” in a week as wholesale power prices skyrocketed from around $50 to $2,000–$7,000 per MWh. Management warned that an hour longer offline could have caused irreversible pot line damage. The root cause was insufficient affordable supply (gas-fired generation sat idle while prices soared), underscoring how tight gas and power markets directly threaten heavy industry.[28]

Likewise, the Portland aluminium smelter in Victoria nearly closed in 2021 amid untenable energy costs, until a government-backed rescue package of over $150 million was arranged to secure a cheaper electricity deal.[29] Portland’s survival required this lifeline to compensate for what high power (and indirectly gas) prices had rendered an unviable operation. Even planned new gas infrastructure has been affected — the Kurri Kurri gas power plant in NSW, slated in 2021 as a government response to supply shortfalls, was scaled back and delayed amid questions of economics and policy changes (it is now expected to run on a limited basis, ~2% capacity).

Several other Australian companies and industrial plants have already reduced operations, paused production, or shut down due to rising gas prices and limited supply, including:

- Incitec Pivot (IPL) closed its Gibson Island fertiliser plant in Brisbane, Queensland, in December 2022 due to high natural gas prices and an inability to secure a long-term gas supply agreement. The closure cost approximately 170 jobs. IPL transitioned to importing fertilisers to replace those previously manufactured at the plant. Its Geelong fertiliser plant in Victoria also shut down due to similar energy cost pressures, costing around 40 jobs.[30]

- Qenos, Australia’s last plastics manufacturer, entered administration and closed its Altona facility in Victoria in 2024. The shutdown was attributed to unreliable and unaffordable gas supply.[31]

- Oceania Glass, the country’s only architectural glass maker, ceased operations in 2025 after nearly 169 years in Victoria, citing soaring gas and electricity costs as a key driver.[32]

- The ACCC’s investigation for its 2023 Gas Shortage report identified Advance Bricks closing its manufacturing operations due to gas price rises.[33]

- The Master Butchers Co-operative MBL Proteins plant saw its monthly gas bill soar from ~$135,000 to $900,000, or nearly a $9 million annual increase — an escalation that threatened its viability.[34]

Each of these cases shows the real-world fallout of scarce and expensive gas supply: major employers either shutting down, requiring subsidies, or struggling to justify new investments. The broader manufacturing sector has similarly suffered, with energy-intensive factories (fertilisers, glass, brickworks, etc.) cutting output or relocating due to Australia’s high gas costs. The de-industrialisation pressure is mounting as gas prices remain elevated.

These closures and cutbacks reflect how escalating gas prices and volatile contract terms are not just cost issues — they are causing permanent loss of domestic industrial capacity. The manufacturing sector’s decline — from around 14% down to ~5% of GDP[35] — is significantly influenced by energy cost competitiveness and gas supply insecurity. ACCC and energy policy reviews emphasise that without stronger domestic gas reservation and pricing safeguards, more closures could follow, especially among energy-intensive manufacturers.[36]

Exports and security

Australia’s reduced domestic gas supply could also pose a significant threat to its gas export contracts, if it results in the domestic need cannibalising exports. This could become a national security issue, particularly when it disrupts supplies to key allies such as Japan, which is one of our major gas markets. The demand for Australian LNG is high largely because Japan relies heavily on our imported natural gas to meet its energy needs, especially following the closure of its nuclear reactors after the 2011 Fukushima disaster. Consequently, Australia’s role as a key supplier of gas is crucial to Japan’s energy security and economic stability. A reduction in Australia’s domestic gas due to factors like decreased production may see us struggle to meet export commitments, which would undermine our reliability as an energy supplier to our allies.

History

Until the 1960s, natural gas was largely treated as a waste product of oil production and was often flared. In Australia, its first significant use was as a substitute for toxic town gas and later for electricity generation. Major cities converted gradually: Melbourne secured long-term supply from Bass Strait in a favourable deal, while Sydney lagged until the Moomba pipeline brought supply in 1976.[37]

Government interventions often slowed progress. In Western Australia, Premier Charles Court attempted to drive petrochemical development by reserving North West Shelf gas. The Dampier-to-Perth pipeline, built under government control, ran vastly over budget. In contrast, private enterprise delivered a pipeline from Alice Springs to Darwin on time and at cost. By the mid-1980s, natural gas was widely available in major centres and regional industrial hubs, although coal remained dominant in electricity generation.[38]

The 1970s and 1980s marked the rise of gas pioneers. Consortia led by Woodside developed vast offshore fields in WA, launching the North West Shelf project, which established both export and domestic supply infrastructure. On the east coast, Santos developed the Cooper Basin, building pipelines to Adelaide and Sydney. Governments acted mainly as facilitators, with private investors driving exploration and infrastructure.

During the 1990s, economic reform reshaped the market. Under National Competition Policy, pipeline monopolies were broken up, and third-party access rules created more competitive domestic markets. At the same time, Australia’s LNG export industry expanded from the North West Shelf to new projects such as Gorgon, Pluto, and Darwin LNG, all backed by private capital. WA introduced a formal domestic gas reservation policy in 2006, requiring 15% of LNG output to be reserved for local use. This policy kept WA prices stable and significantly lower than on the east coast.[39]

On the east coast, by contrast, governments did not impose reservation requirements. In the late 2000s, Queensland pioneered CSG-to-LNG projects, building three export plants at Gladstone. This linked domestic prices to international markets. From 2015, as exports ramped up, domestic prices surged, sparking political backlash. The federal government introduced the Australian Domestic Gas Security Mechanism in 2017, threatening to restrict exports unless domestic needs were met.[40]

The 2010s saw further conflicts between supply ambitions and environmental opposition. Projects such as Narrabri faced long delays due to community resistance,[41] while Victoria banned fracking outright.[42] Meanwhile, WA’s reservation policy insulated its consumers from price spikes afflicting the east coast.[43]

In the 2020s, crises intensified as global shocks — notably the war in Ukraine — pushed gas prices to record highs.[44] Governments imposed temporary price caps and created a mandatory code of conduct to secure domestic supply. Fiscal motives also became prominent, with reforms to resource taxes and states benefiting from royalty windfalls.[45] See Appendix for a more detailed history of gas in Australia.

Current policy proposals

In 2025, Australia stands at a crossroads. After decades of constraining gas development the government has finally concluded that natural gas should play a role in the energy equation. East coast governments are now considering adopting domestic reservation policies once thought unworkable, while industry warns that heavy-handed interventions risk undermining future investment.[46] The central tension remains between ensuring affordable domestic supply and maintaining confidence in Australia as a secure destination for global gas investment.

Further interventions in the natural gas industry are under review to correct this. The federal government launched a sweeping review of gas market regulation in 2025, openly considering more permanent mechanisms to ensure domestic supply, including the once-taboo idea of a formal east coast gas reservation for future projects.[47]

This marks a significant political shift; even the Coalition (traditionally pro-market) campaigned in 2025 on implementing a domestic reservation policy,[48] indicating how politically salient gas prices have become. At the same time, the industry continues to caution that unpredictable rules — be it sudden price caps or export restrictions — risk undermining investment confidence.[49] Former Labor resources minister Joel Fitzgibbon, who is pro-industry, recently warned that “changing the rules mid-game” through retrospective interventions creates sovereign risk and deters the very investment in supply that Australia needs.[50] This tension between short-term political fixes and long-term investment signals remains a central challenge.

Policy impact and future outlook

Forward-looking modelling paints a concerning picture if current policies persist. Frontier Economics (2024) projects that under existing state moratoria (which restrict onshore gas development), Australia’s east coast could face a 15% domestic gas shortfall by 2030 — meaning demand 15% above available supply. This aligns with warnings from market regulators: the ACCC and AEMO have repeatedly cautioned of impending gaps.

AEMO’s 2024 Gas Statement of Opportunities (GSOO) forecasts that without new supply, seasonal gas shortfalls could emerge by winter 2026–27, expanding into year-round supply gaps from 2028–29. In other words, within just a few years the east coast may struggle to meet peak winter demand and even total annual demand, unless new projects (or LNG import terminals) come online. Policy delays are a key factor — for instance, the Narrabri gas project in NSW (which could supply up to 50% of the state’s needs) has been slowed by legal challenges and was only recently reaffirmed by regulators in 2025 after a decade of fighting. Each year Narrabri is postponed keeps upward pressure on prices and forces NSW to import gas from Queensland or overseas.

Longer term, the transition to net-zero will require firming capacity to back up renewables — and here too gas is slated to play a pivotal role.[51] AEMO’s 2024 Integrated System Plan (ISP) finds that maintaining reliability through 2050 will necessitate “gas-fired generation capacity to increase from 11.5 GW now to 15 GW in 2050,” replacing retiring coal units and providing peaking power.[52] In effect, about 6.5 GW of new gas turbines are needed by mid-century to firm solar and wind.

However, current government policies like the Capacity Investment Scheme exclude gas power from incentives, and some states have signalled bans on new gas plants — moves that could leave a critical firming gap.[53] Analysts warn that failure to build the required gas backup would heighten the risk of blackouts, with some estimates of $2–5 billion per year in economic costs if widespread outages occur.[54] AEMO itself has cautioned that accelerating coal closures without sufficient replacement could lead to load shedding events lasting up to 24 hours in a worst-case system-blackout scenario[55] — an outcome to be avoided at all costs. In simple terms, not developing adequate domestic gas supply and generation capacity could impose massive costs on the economy via energy insecurity.

On the flip side, sensible policy reforms could alleviate the crunch. Removing blanket moratoria, streamlining approvals for projects (with appropriate environmental safeguards), and incentivising gas storage and pipelines would encourage new supply to come online faster. The NSW Treasury has argued that expediting projects like Narrabri would not only add significant state revenue and jobs, but also avoid the deadweight losses associated with artificially constrained gas availability.[56]

Similarly, the federal government’s own National Gas Infrastructure Plan identified that a combination of local production (e.g. Narrabri) and infrastructure (e.g. an LNG import terminal or expanded pipelines) “eliminated both annual and peak day shortfalls in southern states”[57] — highlighting that policy choices can indeed bridge the supply gap. Frontier Economics’ modelling for the east coast gas market suggested that a proactive supply strategy (including easing restrictions) would significantly mitigate the forecast shortfall and even contribute to lower wholesale prices over time.[58] In sum, the path forward is a policy choice: continue down the interventionist route that suppresses supply and courts shortages, or adopt a more balanced approach that facilitates investment in gas as a transition fuel, protecting consumers and industries.

Australia’s natural gas sector has been shaped in recent years as much by politics as by geology or markets. Government intervention — in the form of moratoria, protracted approvals, price controls, and mixed signals on new developments — has created a tightrope energy situation. The evidence is clear: underinvestment in gas supply has driven up prices (hurting households and industry), reduced our buffer of reserves, and left the east coast facing foreseeable shortfalls. Large employers like smelters have teetered on the brink due to energy costs.

The very policies intended to manage the transition and protect consumers in the short term (such as price caps or project bans) may be sowing the seeds of greater pain in the medium term by deterring the investment needed for affordable, reliable energy. A balanced policy reset — one that acknowledges gas’s continued role in the near-term energy mix and works to unlock supply in a timely way — is urgently needed. Otherwise, Australia risks a scenario of ‘too little, too late’ on gas: where we neither meet our emissions targets (due to lack of firming capacity) nor safeguard our economy from energy shocks. In the politics of pressure surrounding natural gas, the lesson is that energy security and economic competitiveness hang in the balance of policy decisions. It is time to recalibrate those decisions toward enabling supply, moderating prices, and securing a smoother energy transition.

Balancing public goals with private delivery

Five decades of Australia’s gas development reveal a core lesson: the most effective outcomes occur when public policy goals are aligned with the efficiency and capital of the private sector. Private companies have proven adept at discovering resources, deploying capital, and building projects at immense scale — from the North West Shelf to the CSG terminals, industry initiative turned Australia into an energy powerhouse. Governments achieved the most durable gains when they set clear, consistent rules that harnessed this private capacity toward public ends.

Western Australia’s experience is instructive: by embedding a domestic supply obligation from the outset of LNG projects, WA secured local benefits (low prices and supply for industry) without scaring off investment. Indeed, LNG proceeded and WA enjoyed decades of gas-driven growth. The policy was effective largely because it was stable, transparent, and agreed upon before billions were sunk into infrastructure, allowing companies to factor it into their plans. In contrast, the east coast’s reactive measures (like sudden export controls and price caps) were implemented after crises hit and contracts were signed, which undermined investor confidence and addressed symptoms rather than root causes.

Going forward, Australia can draw several key insights to better balance strategic public interests with efficient private delivery.

Provide policy certainty and avoid knee-jerk changes

Investors in gas (or any energy infrastructure) require long-term certainty given the large upfront costs. Frequent or ad hoc rule changes — for example, retrospective caps on prices or unexpected tax hikes — heighten perceived sovereign risk and can deter the very investments in supply or new technology that would benefit Australia . Governments should strive to set policies through consultative processes and stick to them barring truly extreme circumstances. Mid-course corrections, if needed, should be signalled well in advance. The 2022 emergency price cap, while arguably justified by a war-driven crisis, should remain a rare exception rather than a new normal in regulatory behaviour.

Plan interventions strategically, not defensively

Rather than intervening only when problems reach crisis levels, governments can anticipate issues and shape markets proactively in partnership with industry. For instance, if ensuring domestic gas supply at reasonable prices is a national goal, it would be more effective to design a long-term mechanism (such as a modest reservation on future fields or a strategic storage reserve) now, with input from companies, than to impose blunt instruments later.

Strategic planning could also mean investing in enabling infrastructure — e.g. pipelines connecting new gas basins or supporting pipeline capacity expansions — to alleviate bottlenecks before they become shortages. Another example is streamlining approvals: reducing unnecessary delays in environmental assessments (without sacrificing rigour) would lower project costs and encourage responsible development, benefiting supply in the long run. By being proactive, governments can guide outcomes (like energy security or emission reduction) while providing industry a clearer road map of expectations.

Use market-based tools where possible

There is merit in letting market signals drive efficiency, as long as basic conditions for competition are met. Policies that improve transparency and competition — such as gas trading hubs and pipeline capacity markets — can alleviate issues without heavy-handed control. For example, the creation of the Wallumbilla Gas Hub in Queensland (Australia’s nascent equivalent to the Henry Hub) was a positive step to facilitate gas trading and price discovery.

Likewise, requiring producers to transparently offer gas domestically (as the current code does) or ‘use-it-or-lose-it’ conditions on exploration licenses to prevent land-banking are interventions that still leverage market principles. They encourage private actors to put resources to efficient use or relinquish them to others who will — aligning private profit motives with the public interest in supply. Where direct intervention is necessary (e.g. in emergencies), it should ideally be designed to mimic a market outcome — for instance, a strategic reserve that releases gas when prices exceed certain thresholds, which can calm prices while still allowing normal market operation most of the time.

Align interventions with clear public objectives

Any government action should be grounded in a clear rationale — whether it’s protecting consumers, safeguarding the environment, or ensuring long-term supply — and be evidence-based. This sounds obvious, but clarity of purpose can prevent policies from being pulled in contradictory directions. If the objective is lowering consumer prices, then measures should directly address price drivers (e.g. facilitating new supply or improving competition), rather than politically appealing but tangential moves.

If the goal is decarbonisation, policies should focus on managing the transition (e.g. supporting low-carbon gas production, CCS, or alternatives for gas in industry) rather than simply punishing gas activity in one jurisdiction which can lead to shifting problems elsewhere. By tying interventions to explicit, measurable outcomes (and reviewing their effectiveness regularly), governments can adjust course rationally and maintain trust with both industry and the public.

Collaboration and trust between sectors

Finally, a constructive relationship between government and the gas industry is essential. The narrative of the past decades has sometimes been adversarial — with industry accusing government of hostility or unpredictability, and government officials accusing companies of price gouging or failing to supply the domestic market. Bridging this gap through formal consultation bodies, transparent data sharing (e.g. producers sharing supply forecasts with regulators), and even public-private partnerships on infrastructure could improve outcomes.

For instance, during the 2017 crisis, the ACCC’s ongoing gas market monitoring and its role as an honest broker helped rebuild some trust; the watchdog’s reports highlighted the need for more supply and informed the design of agreements with LNG exporters. When each side understands the other’s constraints — companies need profit to invest, governments need reliability and public acceptance — policies can be crafted that satisfy both. A future example could be co-designing a domestic reservation for new fields that still guarantees exporters a decent return, or coordinating timed development of gas and renewable projects to smooth the transition.

Conclusion

The story of Australia’s natural gas sector is ultimately one of private dynamism tempered by public interest — or more strongly: private initiative shaped, and often distorted, by political intervention.

The pendulum of policy has swung between laissez-faire and intervention, often in response to the pressures of the moment. Over five decades, governments have oscillated between enabling and constraining industry, with the most durable successes arising when stable, transparent frameworks aligned public objectives with private capacity. Where policy has been reactive or inconsistent—whether through moratoria, retrospective price caps, or sudden export restrictions—the results have been costly delays, reduced investment, and growing risks to supply security.

The challenge ahead is to take the lessons learned — from WA’s stable policy to the east coast’s cautions — and establish a framework where the private sector can confidently deliver investment and innovation, while the public interest is safeguarded by thoughtful, consistent policy.

Achieving this balance will be crucial, not only for avoiding the ‘boom-bust’ and crisis cycles of the past, but also for navigating the broader energy transition as Australia aims to secure affordable, reliable energy and meet climate goals.

The evidence presented in this paper demonstrates that unless Australia recalibrates its approach, the nation faces a dual challenge: structurally higher energy costs undermining industrial competitiveness, and insufficient firming capacity to secure the renewable transition. Avoiding this scenario requires a deliberate reset of policy settings, guided by the following principles:

- Policy certainty: investors must be able to rely on clear, predictable rules. Emergency measures such as price caps should remain rare exceptions, not recurring instruments.

- Strategic interventions: governments should anticipate bottlenecks and design long-term mechanisms, such as modest domestic reservations on new fields, or investment in strategic storage and enabling infrastructure.

- Market-based tools: interventions should encourage efficiency and transparency, for example through gas trading hubs, pipeline access reform, and ‘use-it-or-lose-it’ licence conditions.

- Clarity of objectives: policies must be grounded in explicit, evidence-based goals — whether to lower prices, ensure security, or manage emissions — so that interventions directly address these ends.

- Collaboration and trust: enduring outcomes depend on constructive engagement between governments and industry, underpinned by transparent data and co-designed solutions.

Western Australia’s experience shows that well-designed, stable policies can secure domestic supply without deterring export investment. The east coast, by contrast, illustrates the perils of ad hoc, politically motivated interventions that chase symptoms rather than causes. Going forward, Australia must emulate the former rather than repeat the latter.

Key policy proposals to achieve this:

- Lift Bans and Moratoria: Remove or relax state-level prohibitions and moratoria on onshore gas exploration and unconventional extraction (such as CSG and fracking), which have stalled new supply and deterred investment.

- Accelerate Approvals: Streamline and speed up project approval processes, especially environmental assessments, to reduce delays and costs while maintaining safeguards. Prioritise fast-tracking delayed projects such as Narrabri and Beetaloo to avert projected supply shortfalls.

- Introduce a Stable Prospective Domestic Gas Reservation Policy: Consider implementing a formal domestic gas reservation on the east coast (similar to Western Australia’s model) to ensure a portion of new production is set aside for domestic use, giving industry price stability while maintaining export capacity.

- Provide Long-Term Policy Certainty: Avoid retrospective or ad hoc interventions (such as sudden price caps or export restrictions) that create sovereign risk and deter investment. Develop clear, consistent and consultative policy settings to support investor confidence.

- Plan Strategic Interventions: Shift from reactive crisis responses to proactive planning. For example, establish strategic gas storage reserves, expand pipeline capacity, and invest in infrastructure that connects new gas basins to demand centres before shortages emerge.

- Use Market-Based Incentives: Where possible, rely on market mechanisms and competitive signals to allocate resources efficiently, while ensuring the regulatory framework allows fair competition and investment returns.

- Recognise Gas as a Key Transition Fuel: Explicitly incorporate new gas-fired generation into long-term energy planning to provide firming capacity for renewables, in line with projections from AEMO that additional gas generation will be required to maintain reliability to 2050.

With better foresight and cooperation, Australia can harness its private sector strengths to meet public needs, ensuring that the politics of pressure give way to a politics of pragmatic partnership in the natural gas domain.

If policymakers can achieve this recalibration, the gas sector can continue to provide affordable energy, industrial competitiveness, and the firming capacity required for decarbonisation. Failure to do so will leave Australia exposed to energy shocks, economic decline in key industries, and a more disorderly energy transition. The choice is clear: to move beyond the politics of pressure and embrace a politics of pragmatic partnership that balances public needs with private delivery.

Appendix – History of gas in Australia

Up until the ‘60s, natural gas was a waste product of the oil business. Oil production generated associated gas which was a problem for the industry. Sometimes gas can be re-injected to improve oil flow but largely it was flared.

In Australia, natural gas started to be used as feedstock for substitution for domestic town gas and later electric power generation. Town gas was a toxic mixture of CO, hydrogen, CO2, methane, and nitrogen. The switch to natural gas caused problems with pipe leaks and the need to change appliances.

Brisbane, Perth and Adelaide were converted and Melbourne benefited from a deal done by the premier Henry Bolte to receive gas from the Bass Strait oil production for free at the Sale separation plant. This arrangement lasted for nearly 30 years.

Sydney lagged the other states as NSW had no gas production. AGL eventually secured supply from the Moomba fields in South Australia. Its largest customer was a fertiliser plant near Newcastle. Unfortunately, with the election of the Whitlam government, the energy minister Rex Connor decided the government would create a national grid for natural gas and nationalised the gas pipeline to Sydney. This caused several years of delay but gas eventually arrived in 1976.

In the west, government again intervened. Charles Court, the premier, wanted to develop a petrochemical plant in Kwinana south of Perth and decreed that NW Shelf gas, which was being developed as an export project, should be partially reserved for his petrochemical ambitions. Again, several years passed before the proponents could firm up a plan. Governments were generally ignorant of the skills needed to develop long distant pipelines.

The West Australian government refused industry help and commissioned the State Electric Commission (SECWA) to build the line from Dampier to Perth largely for the petrochemical development. Alcoa was forced to buy half the gas to help pay for the gas transmission costs. SECWA in turn hired an iron ore specialist to manage the project who in turn contracted a water pipeline specialist from Korea. They gave the job to Koreans as they hoped the Koreans would finance the petrochemical plant. The project came in at double the budget, $1.2 billion. In parallel to this a gas pipeline was built from west of Alice Springs to Darwin on budget and on time. This was done by private enterprise with industry specialists.

By the mid ‘80s natural gas was available in most major centres and larger rural towns. Laterals had been built through central WA from the North West Shelf reserves to feed mining operations and power plants. In Queensland, a pipeline was installed to Gladstone from the Roma area for the industrial plants. Also, the central west in NSW was served by a pipeline running north from Young to Tamworth. All of these projects were driven by industrial needs such as brickworks.

Electricity generation in Australia was largely facilitated by burning coal. Australia had large reserves of brown coal in Victoria and extensive high quality black coal in NSW and QLD. SA and WA had limited reserves and relied on diesel generators in the country regions as did the NT. Over the past century or more transmission and distribution systems were installed to connect the customers. By the 1980s cheap coal created low-cost energy for most of the country facilitating large industrial development for the export of aluminium and steel. Householders had access to the cheapest power in the world.

Pioneers of the gas industry (1970s–1980s)

In the early 1970s, consortia led by Woodside Petroleum discovered huge gas fields off Western Australia’s north-west coast (the North Rankin, Goodwyn, and Angel fields). Developing these resources was technically challenging and capital-intensive — by the late 1980s the North West Shelf project had grown into one of the world’s largest engineering undertakings, with investment exceeding A$25 billion. This venture built the Karratha gas plant, offshore platforms, and a pipeline to bring gas onshore. Crucially, it also established infrastructure for both export and domestic supply: the first phase of the North West Shelf in the early 1980s included a pipeline delivering gas to Western Australian consumers as early as 1984.

Private companies similarly spearheaded east coast development. In the Cooper Basin (South Australia/Queensland), joint ventures led by Santos discovered gas in the 1960s, prompting construction of a pipeline to Adelaide. By 1976, the 1300 km Moomba-to-Sydney pipeline was completed.

Governments acted mainly as facilitators — issuing licenses, acquiring easements for pipelines, and sometimes owning downstream utilities that purchased gas. Pricing of domestic gas was administered by state regulators or state-owned distributors. Overall, however, the late 20th-century gas expansion was led by private explorers and investors, with government support largely taking the form of enabling infrastructure or market access.

Market expansion and policy responses (1990s–2000s)

By the 1990s, Australia’s gas sector was growing in both scope and complexity. Private enterprise continued to drive expansion — discovering new fields and proposing ambitious export projects — while governments increasingly turned to regulatory frameworks to control the developing market. A wave of pro-market reform swept through Australia’s energy policies in the 1990s: under National Competition Policy, governments introduced a third-party access regime for gas pipelines, breaking up pipeline monopolies to encourage competition. Private pipeline companies proliferated, building links such as the Eastern Gas Pipeline (connecting Bass Strait gas to NSW) and others, under a new regime where pipeline owners had to provide open access to competitors. The intent — to rely on market competition to deliver efficiency and lower prices — was rooted in the economic liberalism of the era. In practice, these reforms did spur a more dynamic domestic gas market, with multiple suppliers and traders emerging. However, they also required government involvement in setting the rules (e.g. the 1997 National Gas Pipelines Access Code), illustrating that even ‘free market’ expansions were steered by policy frameworks.

During the same period, the seeds of Australia’s LNG export industry began to germinate. Building on the success of the North West Shelf (which shipped its first LNG cargo in 1989), private consortia proposed new export terminals. Through the 2000s, international oil and gas companies invested in mega-projects across northern Australia: the Gorgon LNG project led by Chevron in WA, Darwin LNG drawing on Bayu-Undan field, and Pluto LNG by Woodside, among others. By the end of the 2000s, Australia was set to massively expand LNG capacity — entirely funded and constructed by the private sector, which by then had decades of technical expertise in offshore development. Governments largely welcomed these investments for the export revenue, jobs, and royalties they promised.

Western Australia, having established an informal domestic supply rule decades earlier, formally codified its Domestic Gas Reservation Policy in 2006, just as new LNG projects were taking off. The policy requires LNG exporters in WA to make the equivalent of 15% of their LNG production available to the WA domestic market. This was a strategic intervention: WA’s leaders (of all political stripes) believed that reserving a share of gas for local use would foster industry and keep prices in check for consumers. The reservation condition was written into project approvals for developments like Gorgon and Wheatstone LNG. While industry initially resisted, it ultimately complied in order to secure licenses — exemplifying how government could leverage its approval powers to extract public-interest commitments from private developers. Politically, WA’s stance was driven by a pragmatic, state-development ideology: even pro-market politicians in WA saw domestic reservation as insurance against gas shortages in a state isolated from the east coast grid. Over time, this policy proved significant: gas prices in WA have remained roughly half the levels of east coast prices since 2015, a disparity widely attributed to WA’s reservation policy ensuring local supply. However, the WA Domestic Gas Policy Inquiry over in the past few years found that the state’s domestic gas commitment agreements suffer from vague and inconsistent terms that undermine effective enforcement. Key findings highlighted that flexible delivery schedules allow producers to delay supply, while the poorly defined “marketing in good faith” obligation is too imprecise to monitor or enforce. The Inquiry noted that enforcement powers vary between agreements and often rely on private arbitration rather than public oversight, leaving the state with limited leverage to ensure reliable domestic gas supply. It also observed that some producers were not acting in the spirit of the policy, reinforcing the need for measurable obligations, transparent reporting, and enforceable penalties. Overall, the Inquiry concluded that clearer, standardised contracts and a consistent compliance and penalty framework are essential to secure the intended domestic gas outcomes.[59]

On the east coast, however, the 2000s unfolded very differently. No formal reservation policy was instituted for new projects, reflecting the federal Coalition government’s free-market ideology at the time. The Howard Government (1996–2007) and its state counterparts — and the federal Labor government in the late years of the decade — largely believed that requiring gas for domestic use would deter LNG investment. Instead, they trusted that market forces and increasing supply would keep domestic gas abundant. This approach faced little immediate test in the 2000s because the east coast had not yet started exporting LNG — domestic gas remained relatively cheap and available from existing fields in Bass Strait and the Cooper Basin. Indeed, through the early 2000s manufacturers enjoyed long-term gas contracts at prices often in the $3–4 per giga joule range, and new retail competition in gas emerged as states privatised gas retailers. Government intervention in this era was thus more about market structure (regulations for competition) than market outcomes like pricing or allocation. An exception was infrastructure facilitation: for instance, federal and state governments occasionally chipped in funds or approvals for pipelines to connect new gas sources to markets (e.g. pipelines bringing gas from Queensland’s Surat Basin to the south).

By the end of the 2000s, private sector ambition was reaching new heights on the east coast: a pioneering plan to export LNG from Queensland’s CSG fields was moving forward. Origin Energy, Santos, and British Gas Group led consortia that sanctioned three LNG export terminals at Gladstone (Curtis Island) around 2010. Together these projects represented around $80 billion in private investment — constructing liquefaction plants and drilling thousands of CSG wells in rural Queensland. It was an unprecedented gambit globally (the first LNG plants fed by CSG) and promised to transform the east coast gas landscape. Government leaders in Queensland eagerly supported this development, motivated by economic growth and royalty revenues. Environmental and landholder concerns were present, but at that time Queensland’s Labor government issued environmental approvals and land access arrangements relatively swiftly, positioning the state as an investment-friendly jurisdiction. In effect, private developers created an entirely new export industry out of the east coast gas supply, with governments playing cheerleader and facilitator.

By the late 2000s, CSG exploration had extended beyond Queensland into New South Wales and Victoria, prompting community backlash (especially from farmers and environmental groups worried about water resources and fracking). As electoral pressure mounted, some state governments intervened to restrict gas development despite industry’s push. Victoria imposed a moratorium on onshore gas drilling in 2012, which evolved into a permanent ban on fracking and CSG by 2017 — a ban later enshrined in the state’s Constitution in 2021. This extraordinary step, taken by the Andrews Labor Government with bipartisan support, was explicitly driven by public sentiment in agricultural regions: “We’ve listened to our rural communities who do not want the unacceptable risks that fracking brings,” declared Victoria’s Resources Minister in 2017. Here, the political motivation was primarily electoral and ideological — maintaining public and environmental trust was deemed more important than potential gas revenue. Similarly, New South Wales introduced stringent exclusion zones that blocked CSG near certain water catchments and sensitive areas, effectively stalling most onshore gas projects in the state. These preventive interventions were early signs that not all government actions sought to accelerate gas supply; some, influenced by environmental and voter concerns, acted to slow or halt development in the name of other public values.

Boom, shortfalls, and backlash (2010s)

The 2010s were a tumultuous decade for Australian gas, as the LNG boom collided with domestic market realities and prompted a flurry of reactive government measures. The culmination of Queensland’s CSG-to-LNG vision saw the first LNG cargo exported in 2015. Within just a few years, three LNG plants were fully operational. Export demand surged so dramatically that by the late 2010s nearly three-quarters of all gas produced on the east coast was being shipped overseas.

This linkage of the domestic gas market to international prices was a watershed moment. Local buyers who once enjoyed gas at <$4/GJ suddenly found themselves competing with Asian LNG prices indexed to oil. By 2018, spot gas prices in eastern Australia frequently spiked above $15/GJ, and contract prices for industrial users more than doubled from pre-LNG levels. Manufacturers warned of plant closures, power generators switched to alternatives where possible, and households felt the pinch in higher gas and electricity bills. Eastern Australia had effectively transitioned from a buyer’s market to a seller’s market, due in part to the success of LNG.

This rapid change took governments by surprise and sparked a backlash. Having earlier rejected a reservation policy, the federal government under Malcolm Turnbull faced mounting public pressure as east coast gas shortages were projected. In 2017, in a striking intervention, the Turnbull Government created the Australian Domestic Gas Security Mechanism (ADGSM) — often called the ‘gas trigger’ — empowering Canberra to curb LNG exports in the event of domestic shortfalls.

The mere threat of pulling this ‘trigger’ brought LNG exporters to the table: the majors (Origin/ConocoPhillips, Shell, and Santos) agreed to divert more gas to domestic users to avoid formal restrictions. A Heads of Agreement was signed in 2017 (and renewed later) whereby LNG operators promised to offer uncontracted gas to Australians first. This episode illustrated the political imperative at play: a Liberal-National government ideologically inclined to free markets nonetheless intervened in an unprecedented way when faced with angry manufacturers, media criticism, and the prospect of voters seeing factories shut for lack of gas. Electorally, it was considered necessary to head off a looming crisis. As then-Prime Minister Turnbull put it bluntly, “we are ensuring Australians have first call on Australian gas” — a nationalist framing that resonated with the public mood.

State governments also reacted. In 2017, facing its own voters’ discontent at rising prices, the New South Wales government struck agreements to accelerate local gas development (such as the Narrabri CSG project proposed by Santos) in exchange for federal support on energy infrastructure. The Narrabri Gas Project became a test case: initially proposed in 2014, it only won state approval in late 2020 after years of protracted environmental assessments and community opposition.

The independent planning commission attached an extraordinary 134 conditions to the approval, requiring phased compliance at each stage. Both federal and state Coalition governments had openly backed Narrabri as key to boosting supply (the project was touted as capable of supplying up to 50% of NSW’s gas demand). Critics alleged political pressure played a role in pushing it through despite environmental concerns. The Narrabri saga exemplifies how government’s desire to increase gas supply (for energy security and regional jobs) ran up against environmental regulation and public opposition — resulting in delays and onerous conditions that even after approval have meant the project has yet to deliver any gas by 2025. In effect, political will managed to get a green light for Narrabri, but only by imposing measures that likely increased costs and uncertainty for the developer.

Meanwhile, the WA domestic gas reservation policy proved its worth during the 2010s. While east coast prices soared with LNG exports, Western Australia — which was simultaneously exporting huge volumes of LNG from new projects like Gorgon and Wheatstone — saw its domestic gas prices remain relatively stable and low. Analyses by the Reserve Bank of Australia found that WA gas prices stayed roughly 50% below east coast levels and did not track international price spikes, thanks to the state’s policy insulating the local market. Industrial users in WA enjoyed gas around $5–6/GJ even as their eastern counterparts struggled with $10+ quotes.

This contrast was not lost in the national debate. Critics of east coast policy argued that if a modest reservation had been in place or if CSG development in southern states had been facilitated rather than banned, the domestic market squeeze might have been avoided. Proponents of free markets countered that WA’s situation was unique (an isolated market with abundant gas) and cautioned that imposing reservation on east coast projects after investment decisions would undermine Australia’s sovereign risk profile. Government correspondence released in 2018 showed intense lobbying by industry against any retrospective reservation, and federal ministers publicly affirmed respect for contracts already signed.

Political motivations during this period often reflected ideology colliding with reality. The Coalition (Liberal-National) governments (2013–2022) were philosophically aligned with resource development and minimising intervention. Yet they found themselves adopting interventionist tools — like the ADGSM export control — out of electoral pragmatism when high gas and electricity prices became a public outrage. State Labor governments, conversely, while more open to market intervention for social or environmental aims, had to confront the economic consequences of restricting gas supply. For example, the new Labor government in Western Australia in 2017 briefly instated a moratorium on fracking pending an inquiry (honouring an election promise to environmental constituencies), but lifted the ban on most of the state in 2018 when the inquiry found risks manageable — keeping in place a fracking ban only in the populated southwest and sensitive areas . This demonstrated a balance between ideology (environmental precaution) and fiscal/economic concerns (not shutting off a whole industry). In the Northern Territory, a Labor government similarly imposed a moratorium on shale gas fracking in 2016, only to lift it in 2018 after its scientific inquiry, given the significant economic opportunity in the Beetaloo Basin (and with plenty of regulatory caveats to show voters it was being done carefully). The common thread was that government interventions in the 2010s were often reactive — responding to short-term crises or political pressures — rather than long-term strategic planning, and this reactivity sometimes exacerbated industry uncertainty.

Crisis and controls in the 2020s

The early 2020s brought new pressure points that prompted even more direct government intervention in gas markets. The COVID-19 pandemic initially caused a slump in energy demand, but as the economy recovered — and especially after Russia’s invasion of Ukraine in 2022 — global energy prices skyrocketed. Australia, with its LNG exports now in full swing, saw domestic gas prices follow the international surge upward. By late 2022, spot gas prices in eastern Australia spiked to record highs (~$30–40/GJ in some instances) amid fear of shortages for the coming winter. This created a genuine energy affordability crisis for many Australian industries and households, and a political crisis for the new Albanese Labor Government (elected 2022) which had campaigned on easing cost-of-living pressures.

Annual domestic demand for gas (excluding gas for electricity generation) is 500 million gigajoules. Today this wholesales at $17.30 per gigajoule, representing a premium of over $13 per gigajoule more than the price prevailing 10 years ago (and $12 per gigajoule over the current US price).

Had governments in New South Wales, Victoria, and South Australia permitted exploration and production (and had the Commonwealth regulations been less restrictive) today’s prices would have been at least $10 per gigajoule cheaper than those now prevailing. Regulatory restraints on gas have therefore brought a cost of some $5 billion a year (500 million gigajoules x $10/gigajoule) to industrial and household consumers.

Confronted with this emergency, federal and state governments took the unprecedented step of capping gas prices by law. In December 2022, the Commonwealth legislated a temporary emergency cap of $12 per gigajoule on wholesale natural gas sales by east coast producers for a period of 12 months. This Gas Market Emergency Price Order applied to new contracts for 2023 (while exempting already-signed agreements and not interfering with export sales).

States cooperated by implementing caps on coal prices simultaneously, in an effort to blunt the energy inflation hitting the economy. The rationale given was straightforward: extraordinary global conditions (exacerbated by the war in Ukraine) had led to windfall gains for gas exporters while Australian consumers were suffering; hence, the government needed to intervene to ‘shield’ families and businesses. Politically, it was a bold move fitting with Labor’s ideological tilt toward market intervention for social outcomes. Electorally, it was seen as critical to show action on power bills.

Industry reaction was swift and negative. Gas producers condemned the price cap as heavy-handed and warned it would chill investment in new supply. Analysts and companies cautioned that imposing price controls (especially if extended or made permanent) could deter the very exploration and development needed to alleviate the supply crunch long-term. The government, cognisant of these arguments, framed the cap as a short-term ‘emergency’ measure and simultaneously unveiled a longer-term mandatory Gas Market Code of Conduct. Under this new code (negotiated in 2023), gas producers must offer domestic buyers reasonable supply terms, with a provision for arbitration and an ongoing price anchor of $12/GJ unless exemptions are granted.

Essentially, the government moved toward a semi-regulated pricing regime for domestic gas, albeit one that can be loosened for producers who commit to domestic supply. This represented probably the most intrusive federal intervention in the gas market’s history. It was driven by a mix of electoral calculus and a dose of fiscal realism — the government argued that unchecked gas prices would damage the broader economy and budget, whereas moderating prices would help temper inflation. In selling the policy, Energy Minister Chris Bowen emphasised protecting families and industry while still providing “certainty for our valued trading partners” in exports, reflecting the political need to appear pro-consumer without scaring off international investors.

On the state level, interventionist policies also persisted. Victoria maintained its ban on fracking and CSG, even as it lifted a moratorium on conventional onshore gas in 2021 to allow some new supply under strict conditions. New South Wales, after approving Narrabri, ensured that gas from that project (if and when it flows) will be reserved entirely for domestic use — a sort of project-specific reservation akin to what Queensland had started doing for certain acreage releases. Queensland itself, while proudly pro-LNG, began carving out new gas blocks that are conditioned for domestic-only sales, effectively creating a partial reservation policy by stealth. These moves show states trying to balance the lure of export revenue with the need to mollify domestic consumers and voters. Western Australia, for its part, doubled down on enforcement of its reservation policy as new projects came online, and thanks to that policy, WA largely avoided the east coast’s crisis — a fact frequently cited in policy debates.

Fiscal drivers became more explicitly part of gas policy in the 2020s as well. Governments, facing budget pressures, looked to the booming gas sector for additional revenue. In 2023 the Labor federal government announced reforms to the Petroleum Resource Rent Tax (PRRT) to “increase the tax paid by the offshore LNG industry” and bring forward roughly A$2.4 billion in revenue over four years. The change, which limits certain tax deductions, was justified on grounds that LNG projects had been paying minimal PRRT and needed to contribute their fair share sooner. Politically this was an easier sell amid reports of record export earnings, but it was not without controversy — industry leaders lobbied against overreach, warning that higher taxes could “undercut future revenue and choke off investment needed to increase supply”.

The government proceeded, calculating that the fiscal upside and public favour from reclaiming resource rents outweighed the risks. State treasuries likewise reaped windfalls from royalties as gas prices spiked; for example, Queensland’s LNG royalties hit record highs in 2022–23, bolstering its budget surplus (a fact not lost on its government as an incentive to keep gas exports flowing). These fiscal motivations often underlie political rhetoric: a government keen on gas development might emphasise jobs and energy security, but the allure of billions in royalties/taxes can be a silent driver for supporting new gas fields or export approvals — or conversely, a target for intervention when public coffers seem shortchanged.

References

Reuters – LNG trade record 2020 (confirming Australia became world’s largest LNG exporter in 2020)

Wikipedia – North West Shelf Project history (noting early 1970s discoveries and scale of investment by late 1980s)

Nat. Library of Australia – Moomba-Sydney Pipeline (construction by Pipeline Authority, completed 1976)

WA Government – Domestic Gas Policy (WA maintained domestic gas policy since underwriting the North West Shelf in 1979)

WA Government – Domestic Gas Policy (15% of LNG exports to be made available domestically in WA)

RBA Bulletin – East Coast Gas Market (WA gas prices ~half east coast levels since 2015, attributed to reservation policy)

ABC News – First LNG from CSG (Qld LNG projects cost ~$60b, first cargo 2015)

Premier of Victoria – Fracking Ban (Vic. banned fracking in 2017, enshrined in Constitution in 2021, responding to farmers/community)

The Guardian – Bowen gas market review (explains ADGSM “trigger” created under Turnbull to restrict LNG exports if shortfall)

The Guardian – Narrabri gas approval (NSW approved Narrabri gas project 2020 with 134 conditions, phased development)

The Guardian – Narrabri gas and gas-fired recovery (Narrabri central to federal “gas-fired recovery”, up to 50% NSW gas demand potential)

The Guardian – Narrabri opposition claims (Lock the Gate claimed political pressure led to inadequate assessment time for Narrabri)

ACCC – Media Release (Dec 2022 federal government introduced 12-month $12/GJ price cap on east coast gas)

Reuters – Gas price cap context (one-year $12/GJ cap approved Dec 2022 to ease pressure on households after Russia-Ukraine crisis)

Reuters – Industry warning (gas producers and analysts warned “reasonable pricing” rules would deter new gas supply investment)

Reuters – PRRT tax changes (2023 reforms to increase LNG industry tax, expected to raise an extra $2.4b over four years)

Reuters – PRRT rationale (most LNG projects not paying significant PRRT until 2030s; changes address this by capping deductions)

Energy Insights blog – Panel discussion (former ministers warn that “changing the rules mid-game” via new controls on gas deters investment)

The Guardian – Gas-led recovery (Morrison championing “gas-led recovery” in 2020, funding $52.9m to boost gas supply and infrastructure)

The Guardian – Industry pushback concerns (Govt wary of pushback and capital flight from imposing formal reservation; opted for negotiation with LNG exporters)

The Guardian – Reservation policies (WA’s 15% reservation since 2006; Queensland’s domestic-only acreage requirements; no east coast-wide regime historically due to political resistance)

ABS Input-Output data (via ACIL Allen analysis) – Estimated annual output of gas-dependent manufacturing (feedstock chemicals) in NSW, showing ~$2.3 billion contribution at risk if gas supply is constrained.

Institute for Energy Economics and Financial Analysis – Key finding noting that since LNG exports began in 2015, domestic gas prices tripled, driving a decline in local gas demand (illustrating the price shock to Australian consumers) and implying significant rises in energy bills.

Australian Energy Producers (APPEA), Election Platform 2025 – Observing that regulatory uncertainty and moratoria have stalled new gas exploration investment. The east coast is now forecast to suffer gas shortfalls from 2027 onward due to lack of supply coming online.

The Guardian (May 2021) – Reporting that the Tomago aluminium smelter in NSW was forced to shut down multiple times in one week, blaming electricity price spikes (from ~$50 to $2,000–7,000/MWh) amid generator outages. Highlights how extreme energy costs nearly froze a critical industrial operation.

ABC News (Mar 2021) – Detailing a government-backed deal of over $150 million to secure a new electricity supply contract for Alcoa’s Portland smelter in Victoria, saving it from closure. The smelter employs 500+ workers and consumes ~10% of Victoria’s power; it needed subsidies to offset high energy prices and ensure its viability.

The Guardian (Apr 2025) – Citing AEMO’s Gas Statement of Opportunities 2024: seasonal shortfalls by 2028 in southern states and annual supply gaps from 2029, absent new development. Reinforces the timeline of projected east coast gas deficits under current policy settings.

Reuters (May 20, 2025) – News on the long-delayed Narrabri gas project: initially proposed over a decade ago, it faced protracted legal battles. A tribunal in 2025 cleared it with conditions, recognising the project’s “important benefit” for domestic energy security despite environmental concerns. (No gas has yet flowed, illustrating the slow project timeline.)

Energy Council summary of AEMO 2024 ISP – The Integrated System Plan calls for increasing dispatchable capacity to firm renewables. Gas-fired generation is projected to grow from 11.5 GW to ~15 GW by 2050 (requiring ~13 GW of new-build gas turbines to replace retiring units and meet new peak demand). This underscores gas’s continuing role as a reliability backbone even as renewables expand.

Australian Financial Review (June 27, 2025) – Reporting AEMO’s warning that a rapid coal exit without adequate firming could lead to major blackouts. In a worst-case “system black” event, households might face up to 24 hours without power, illustrating the scale of economic disruption (potentially billions in losses) if reliable capacity (e.g. gas peakers) is insufficient during the clean energy transition.

NSW Government Future of Gas Statement (July 2021) – Notes that according to the Commonwealth’s National Gas Infrastructure Plan, developing local gas (e.g. Narrabri) plus an LNG import terminal would together avert projected gas shortfalls in southern Australia. Emphasises that additional supply and infrastructure can solve the supply-demand imbalance, a point for policymakers to heed.

Endnotes

[1] https://www.ga.gov.au/aecr2024/gas

[2] ibid

[3] https://www.business.qld.gov.au/industries/mining-energy-water/energy/gas/overview/reserves

[4] https://www.data.qld.gov.au/dataset/petroleum-gas-production-and-reserve-statistics/resource/351e9bd4-d9a1-4d60-a2ed-0e56cae79c4a

[5] https://www.abc.net.au/news/2016-11-22/fracking-permanently-banned-in-victoria/8045264

[6] https://www.acf.org.au/our-work/climate/gas

[7] https://www.legislation.vic.gov.au/as-made/acts/resources-legislation-amendment-fracking-ban-act-2017

[8] https://www.ga.gov.au/aecr2025/overview

[9] https://www.accc.gov.au/media-release/deteriorating-short-term-outlook-for-east-coast-gas-supply

[10] https://www.woodmac.com/news/opinion/how-will-a-20-year-decline-in-exploration-impact-the-outlook-for-energy-investment-in-australia/

[11] https://grattan.edu.au/news/victoria-is-running-out-of-gas-its-a-massive-policy-fail/

[12] https://www.oxfordenergy.org/wpcms/wp-content/uploads/2025/04/Comment-Australia-Gas.pdf

[13] https://www.aemo.com.au/newsroom/media-release/gas-market-outlook-signals-need-for-new-investment

[14] https://apga.org.au/media-releases/urgent-action-needed-to-bring-on-gas-supply-and-keep-australias-economy-moving

[15] https://www.news.com.au/finance/economy/australian-economy/chris-bowen-flags-greater-government-intervention-in-energy-markets-with-gas-market-review/news-story/01f8f1a96c4dc04bbb2373a1f022d1e5

[16] https://www.abc.net.au/news/2024-10-23/tasmania-dry-spell-renewable-energy-boast-under-threat/104500922

[17] https://www.abc.net.au/news/2025-06-30/boyer-paper-mill-coal-to-electric-plans/105472606

[18] https://www.theguardian.com/australia-news/2024/mar/21/southern-australian-households-to-face-gas-shortages-from-2026-as-most-production-set-for-export

[19] https://ieefa.org/articles/export-effect

[20] https://www.nationals.org.au/election-policies/our-plan-to-deliver-australian-gas-for-australians

[21] https://energyproducers.au/fact_sheets/ausgas-econ-contribution/

[22] https://www.nsw.gov.au/sites/default/files/2025-04/tco-a7839363-disclosure-log.pdf

[23] https://www.ussc.edu.au/australias-energy-crisis-americas-energy-surplus

[24] https://www.ga.gov.au/aecr2024/gas

[25] https://www.aer.gov.au/industry/registers/charts/gas-market-prices

[26] https://www.abc.net.au/news/2025-01-13/gas-energy-costs-threaten-manufacturing/104788984

[27] https://www.deloitte.com/au/en/services/economics/analysis/australian-gas-market-transformations.html

[28] https://www.theaustralian.com.au/business/tomago-on-death-row-and-due-to-close-in-2028-with-no-end-in-sight-to-high-energy-costs/news-story/f5aee29c29442eeac108f122bb8f20d3

[29] https://www.abc.net.au/news/2021-03-19/portland-aluminium-smelter-deal-state-federal-governments/13261804

[30] https://www.aumanufacturing.com.au/incitec-pivot-fails-to-secure-gas-supplies-to-close-gibson-island#:~:text=The%20company%20will%20switch%20to,to%20the%20company’s%20forward%20strategy.%E2%80%9D&text=Subscribe%20to%20our%20free%20@AuManufacturing%20newsletter%20here.

[31] https://www.aigroup.com.au/news/media-centre/2024/imminent-qenos-closure-has-massive-implications-for-industry/

[32] https://www.afr.com/companies/manufacturing/private-equity-owned-oceania-glass-goes-bust-after-169-years-20250204-p5l9hv

[33] https://www.abc.net.au/news/2022-06-17/gas-prices-advance-bricks-energy-crisis-regional-jobs/101161446

[34] https://www.abc.net.au/news/2022-06-09/food-processors-warn-gas-crisis-could-shut-them-down/101138228

[35] https://amtil.com.au/weldaustralia-manufacturing-amtil/

[36] https://www.accc.gov.au/about-us/news/speeches/securing-domestic-gas-supply-to-support-our-commercial-and-industrial-users-address

[37] https://www.austlii.edu.au/au/journals/AUMPLawAYbk/1995/18.pdf

[38] https://www.pipeliner.com.au/building-the-dampier-to-perth-pipeline/

[39] https://www.wa.gov.au/organisation/department-of-energy-and-economic-diversification/wa-domestic-gas-policy-development-and-application

[40] https://www.allens.com.au/insights-news/insights/2023/02/government-intervention-in-the-domestic-gas-market-2023-draft-adgsm-guidelines/

[41] https://envirojustice.org.au/press-release/farmers-take-federal-government-to-court-over-narrabri-gas-pipeline-water-risks/

[42] https://www.premier.vic.gov.au/enshrining-victorias-ban-fracking-forever

[43] https://www.theguardian.com/australia-news/2025/jul/08/wa-premier-roger-cook-gas-reserve-policy

[44] https://www.sciencedirect.com/science/article/pii/S0301421523003282

[45] https://ministers.treasury.gov.au/ministers/jim-chalmers-2022/media-releases/new-gas-code-secures-supply-reasonable-prices-australian

[46] https://www.dcceew.gov.au/sites/default/files/documents/electricity-energy-sector-plan-2025.pdf

[47] https://www.minister.industry.gov.au/ministers/king/media-releases/gas-market-review-strengthen-domestic-supply

[48] https://www.liberal.org.au/2025/04/09/australian-gas-for-australians