Summary

Allowing first home buyers to borrow from their superannuation would transform superannuation from an obstacle to home ownership into a vehicle towards it. It would allow individuals to gain security in retirement in a form that better suits their individual circumstances and preferences. However, it would reduce superannuation balances — perhaps by about $11,000 at retirement age, in a central scenario. That would be offset by increased home ownership. Nevertheless, given compulsory superannuation has bipartisan political support, a reduction in balances is an important concern.

Allowing buyers to use their superannuation balances as collateral would have similar advantages to borrowing from super. However, in contrast, it would reduce superannuation balances only in the infrequent and unexpected event of loan foreclosure.

There is a strong case for allowing individuals to access their superannuation balances for worthwhile purposes, such as hardship. This case will grow as contributions increase and the need to save more for retirement diminishes relative to other saving purposes. Alleviating high mortgage payments is one possible use; though other purposes are probably higher priorities.

Each of the above proposals would boost the demand for housing and hence housing prices. They would increase access to housing for the favoured recipients but decrease it for everyone else. Unless supply also increases, they would simply reshuffle a fixed housing stock. So, were measures like these to be considered, they would need to be accompanied by policies that increase housing supply, such as a relaxation of zoning restrictions.

Introduction

This submission discusses whether individuals should be able to use their accumulated superannuation balances to assist in taking out or paying off a home loan.

Paying off a home loan and superannuation are alternative methods of providing security in retirement. The Discussion Paper for Treasury’s 2019 Retirement Income Review notes they constitute two of the three pillars of the Australian retirement system (together with the Age Pension).

Therefore, if an individual wishes to achieve security in retirement by paying off a mortgage, instead of by accumulating superannuation, it is not clear why the government should interfere with that choice.

Moreover, owning a home is an important aspiration in Australian culture. Governments from different jurisdictions and different parties have enthusiastically encouraged it. That reflects a mix of perceived benefits to the buyer and to broader society. Allowing borrowers to use their superannuation to assist in buying a home would be a method of assistance that does not involve a direct cost to the taxpayer.

Furthermore, there are frictions and obstacles to access finance for housing, which superannuation may be able to reduce.

This submission discusses three different policies aimed at addressing these issues:

- Borrowing from superannuation;

- Using superannuation as security for home loans; and

- Placing superannuation in mortgage offset accounts.

These proposals help, in varying degrees, to achieve the objectives above. However, they also have a common limitation. They all improve access to finance and hence boost the demand for housing. Unless the supply of housing increases, this will increase housing prices, aggravating housing affordability. For this reason, the Falinski Report, among others, explicitly noted that any policies that make it easier to buy housing would need to be coupled with measures to increase supply. Specifically, the Falinski Report called for a relaxation of planning restrictions to allow greater housing density.

The context for this inquiry is a crisis of housing affordability. Australia has some of the most expensive housing in the world, especially in our largest cities. Sydney and Melbourne are the third and sixth least affordable housing markets of the 92 international cities surveyed by Demographia.

This damages our economy and reduces our quality of life. For what people are paying, they could instead have several extra rooms and a much shorter commute. Workers are moving away from the best-paying, most productive jobs. Homelessness and inequality are high and rising. Potential homebuyers are trapped in insecure rental accommodation or are forced to remain living with their parents. The home-ownership rate is falling quickly, particularly among young families.

Given that background, this inquiry is well-timed and well-motivated. It is vital that we, as a society, consider a wide range of options for dealing with the crisis. The CIS has argued the key reform needed is a relaxation of planning restrictions. That is primarily a state government responsibility, however, the federal government should provide encouragement and financial assistance. Reform of superannuation may also play a role, but this will be minor.

The rationale for compulsory superannuation

Changes to the system of compulsory superannuation need to recognise the reasons for that system. These arguments are strongly contested but they need to be addressed.

First, is paternalism. There is strong evidence that people tend to be short-sighted – placing inadequate weight on the distant future. So they make inadequate provision for their retirement, a decision they later regret. Compulsory superannuation is intended to make a decision for people that society and their later selves will regard as in their own interest.

Second, superannuation partially displaces collective provision of retirement incomes with self-reliance. Society does not want retirees to be destitute, so provides an old-age pension at taxpayer expense. This can be thought of as providing insurance, and — like any insurance — it creates moral hazard. In this case, it reduces incentives to work and save. Compulsory self-provision is better for work incentives. The taxes that fund the old-age pension reduce incentives to work. The disincentive would be less if those dollars were going to fund the worker’s own retirement (in contrast to other people’s retirement). People will work harder for their own benefit than they will for others.

An overlapping but distinct argument is fiscal sustainability. Reductions in spending on the old-age pension would, in themselves, improve the federal budget balance; which, in turn, is desirable if it reduces the need for distortionary or confiscatory taxes. That benefit must be balanced against the distortionary implications of how one reduces the pension. For example, reducing the pension by increasing tax concessions to private saving reduces the fiscal benefit (though it might be desirable for other reasons).

Against these objectives of compulsory superannuation, there are also costs.

Superannuation reduces taxes on income when it is received and saved. Some see this as concessional. Others see it as moving to a more efficient expenditure base for taxation, offsetting other biases in the tax system. When compared to a (simple but distortionary) income tax benchmark, the tax concessions are regressive, favouring those on high marginal income tax rates.

Moreover, compulsory superannuation distorts saving and investment decisions. It prevents individuals allocating income and investment over time and across investments as they see fit. However, as noted above, individuals need not always know what is in their best interest.

A large part of the rationale for using superannuation for housing is that it helps achieve the objectives of the superannuation system, while avoiding some of the disadvantages.

Promotion of home ownership

A separate rationale for using superannuation for housing is that it facilitates home ownership at little cost to the taxpayer.

Owning a home is an important aspiration in Australian culture; and many want to assist and promote it. It is common to financially assist family members purchase a home. This partly reflects a desire to help the next generation at an important, but sometimes difficult, stage in their lives. More broadly, governments from different jurisdictions and different parties have enthusiastically encouraged home purchase, for example through first homeowner grants.

Whether they should do so is controversial. Home ownership has external benefits. Owners tend to have more civic engagement, they better maintain their garden, they contribute to local public goods and so on. However, these external benefits are estimated to be relatively modest (Glaeser and Shapiro, 2003). Homeowners also vote more conservatively than renters, though views presumably differ on the desirability and importance of that.

Home ownership is already heavily subsidised, relative to renting. This includes the exemption of imputed rent from income tax, exemption from land tax, full exemption from capital gains tax, and exemption from the means test for the old-age pension. Subsidies to renters through Commonwealth Rental Assistance and public housing provide a small partial offset.

Many of the claimed benefits of home ownership, such as community participation, are more accurately described as benefits of long tenure. Stamp duty (which is a tax on turnover) already encourages long tenure for homeowners. If promoting tenure was the objective, providing greater security of tenure for rental tenants (for example, by reducing the progressivity of land tax) might be more cost-effective.

It is sometimes argued that barriers to finance reduce home ownership, especially for those from disadvantaged backgrounds. For example, the repayments on a mortgage may be lower than the rent a tenant has reliably been paying, but they are still judged an excessive risk. A difficulty in addressing these objectives is that the underlying market or regulatory failure is not clear, making the argument difficult to assess and appropriate remedies difficult to design.

Descriptive Data

As background, it is useful to provide some empirical context for the proposals discussed below.

Who are First Home Buyers?

The ABS’s Survey of Income and Housing (SIH) provides a profile of first home buyers. In 2019–20 they comprised 38% of recent home buyers. Most (92%) first home buyers owned their home with a mortgage. 87% of their household income came from employee income (presumably subject to superannuation). At the time of the survey, within three years of purchase, the mean self-reported value of their dwelling was $582,100, comprising equity of $201,100 (35%) and outstanding mortgage of $384,400.

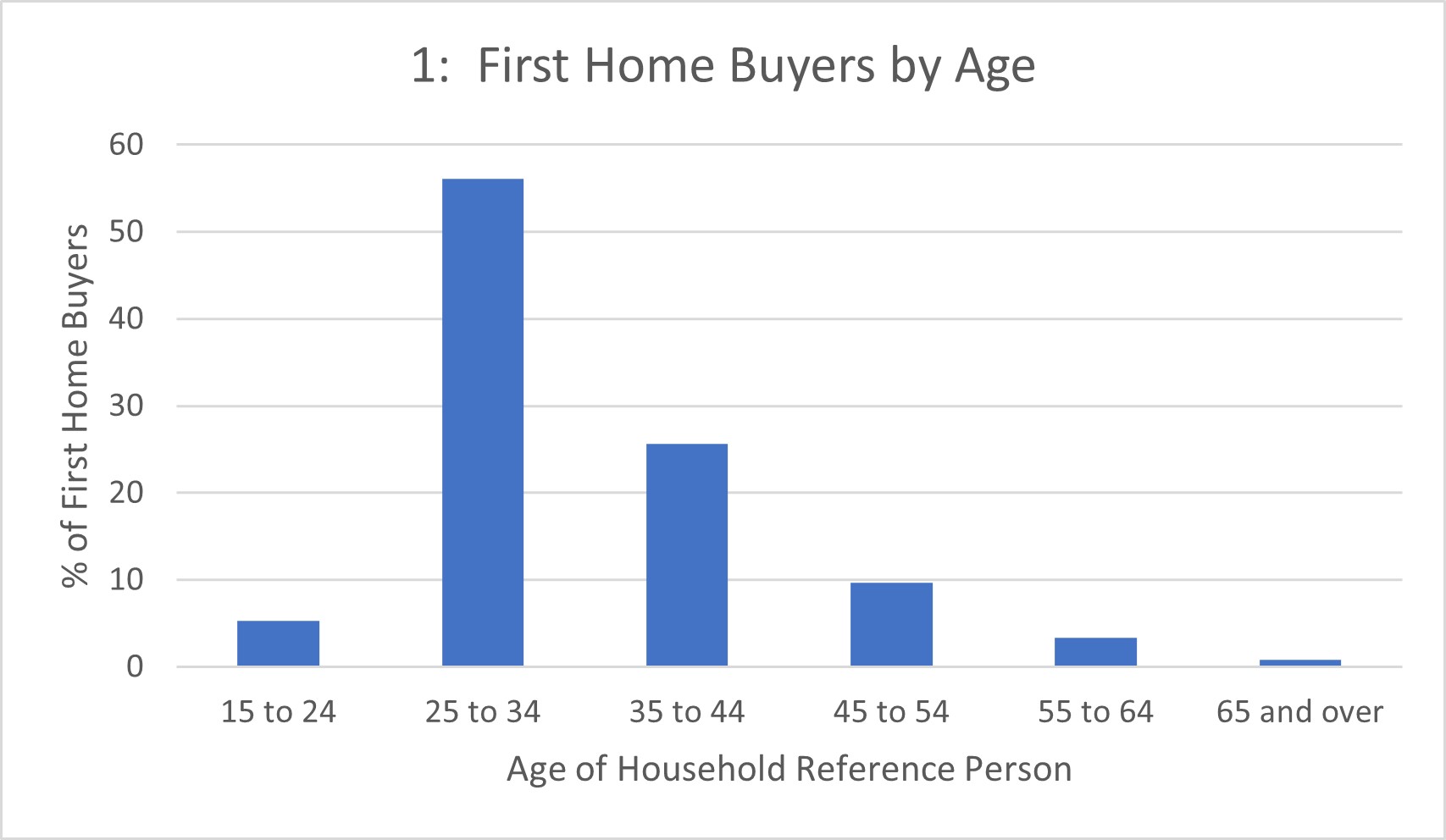

In considering first home buyers’ interaction with superannuation, age is important. As shown in Chart 1, most (56%) were 25-34 years old.

Source: ABS Housing Occupancy and Costs, Australia, 2019–20; Table 9.1

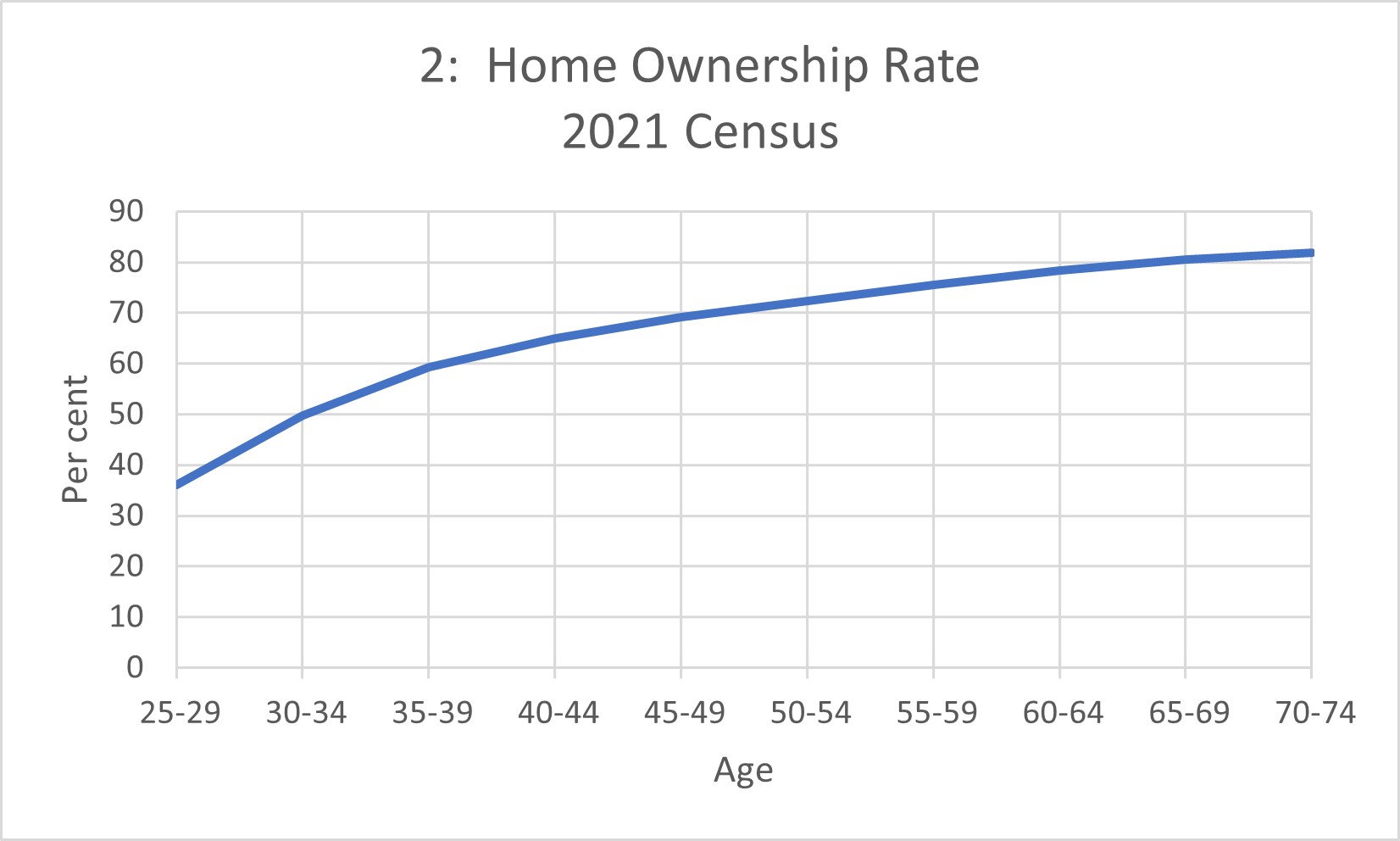

Chart 2 shows home ownership by age. This largely reflects the cumulative sum of the estimates of home buyers above, but also takes sales (and other exits) into account. The median homeowner, in 2021, was 35 years old. As an aside, the relationship in Chart 2 is steeper and lower than in previous years, as ownership has fallen among young households.

Source: ABS 2021 Census, reproduced via AIHW

How much is needed?

According to the ABS “Lending Indicators” release, the average loan to a first home buyer in 2023 was for $501,000 (Table 1).1 Data on deposits of first home buyers is limited. A Commonwealth bank/NHFIC survey estimated that the average first home buyer in 2023 paid a deposit of $159,000 (33 per cent) on a loan of $470,000. Louis Christopher, of SQM Research, estimates “The average first-home buyer, even a couple, on the average household income, would likely take up to 10 years to save a $159,000 deposit”. Equity estimates from the SIH are boosted by repayment of principal and capital gains since purchase, so provide an upper bound.

In any case, deposits paid exceed the required deposit, which is probably the more relevant measure for policy. A deposit of 20% of the principal, or 25% of the loan, is commonly required to avoid mortgage insurance. Using that as a benchmark, the deposit required on an average loan would be $125,000.

Table 1: New Loans to First Home Buyer Owner-occupants

2023

| Average Loan $100,000s |

Assumed Deposit (25% of Loan) |

|

| Australia | 501 | 125 |

| NSW | 607 | 152 |

| Vic | 502 | 126 |

| Qld | 457 | 114 |

| SA | 443 | 111 |

| WA | 417 | 104 |

| Tas | 417 | 104 |

| NT | 412 | 103 |

| ACT | 511 | 128 |

Source: ABS 5601.0 Lending Indicators, Table 24

How large are superannuation balances?

Table 2 shows mean and median superannuation balances by age

Table 2: Mean and Median superannuation balances

2020–21

| Age | Average account balance $ | Median account balance $ | ||||

| under 18 | 9,678 | 238 | ||||

| 18-24 | 7,740 | 4,045 | ||||

| 25-29 | 24,740 | 17,381 | ||||

| 30-34 | 51,400 | 38,681 | ||||

| 35-39 | 86,140 | 65,417 | ||||

| 40-44 | 123,993 | 91,590 | ||||

| 45-49 | 166,937 | 116,886 | ||||

| 50-54 | 215,115 | 137,930 | ||||

| 55-59 | 277,327 | 158,462 | ||||

| 60-64 | 361,539 | 183,524 | ||||

| 65-69 | 428,738 | 207,540 | ||||

| 70-74 | 481,483 | 214,431 | ||||

| 75+ | 475,422 | 171,716 | ||||

| unknown | 13,857 | 7,356 | ||||

| Total | 170,191 | 59,883 | ||||

Source: ATO Taxation Statistics 2020–21, Snapshot detailed tables Table 5; Chart 12.

Comparing Tables 1 and 2, superannuation balances are small relative to the deposit required on a typical first home purchase, even in States with relatively inexpensive housing. For example, putting the median balance of a 30–34-year-old, $38,681 towards a typical first home buyer’s deposit of $125,000 would reduce the remaining deposit by 31%. Putting 40% of the balance towards the deposit, as discussed in Section 5, would reduce it by 12%. That might reduce the time required to save for a deposit from 9 years to 8. So accessing superannuation will have a relatively small effect on deposit hurdles.

Borrowing from superannuation

In the 2022 election, the Coalition parties proposed a Super Home Buyer Scheme. This was modelled on a scheme proposed by Tim Wilson, the member for Goldstein. It would allow first home buyers to withdraw up to $50,000 or up to 40 per cent of their superannuation (whichever is less) to invest in their first home. The scheme would apply to both new and existing homes, with the invested amount to be returned to their superannuation fund when the house is sold, including a share of any capital gain.

While this proposal was widely described as “withdrawing” from superannuation, the funds need to be repaid if and when the property is sold, so it is more accurately described as a loan. Or perhaps more precisely as an equity investment, given that the repayment would comprise a share of any capital gain. It would only be a withdrawal for those who purchase one home in their life and hold it until after retirement.

What might be the effect of this policy on superannuation balances? Consider a typical first home buyer, aged 30-34, with the median superannuation balance for that age group of $39,000 (rounded). Sources for these and following estimates and calculations are shown in the Appendix. In that range, the 40% limit would be the binding constraint, allowing the buyer to borrow $16,000 from their superannuation. According to the ABS’s Survey of Income and Housing, the median time spent in a dwelling by owner-occupiers is ten years (Bloxham, McGregor and Rankin 2010, Graph 3). So assume that the loan is repaid to the superannuation fund after 10 years.

The average 15-year real return on superannuation funds in the accumulation phase, after taxes and investment fees, has been 4.5% per year.2 So one might expect the superannuation account to forgo that return, reducing the balance by $24,226 after 10 years. All these estimates are in constant 2024 dollars.

Partially offsetting this, the loan would be repaid with a share of the capital gains in the house. The average real rate of capital appreciation on Australian housing since 1955 has been 2.4% a year. (Fox and Tulip, 2014). So the initial “equity share” of $15,600 might be expected to grow to $19,775.

Subtracting capital appreciation ($19,775) from typical superannuation returns ($24,226), the superannuation account would be $4,451 lower. Holding other things equal, that would accumulate to $10,734 (in 2024 dollars) over the following 20 years, when the borrower would be near retirement age. This represents the reduction in resources available for retirement. For comparison, the median superannuation balance of 60-64 year-olds was $183,524 (Table 2).

While superannuation balances might be $10,734 lower, home ownership might be expected to be higher. Indeed, that is the point of the policy. However, quantifying this is difficult.

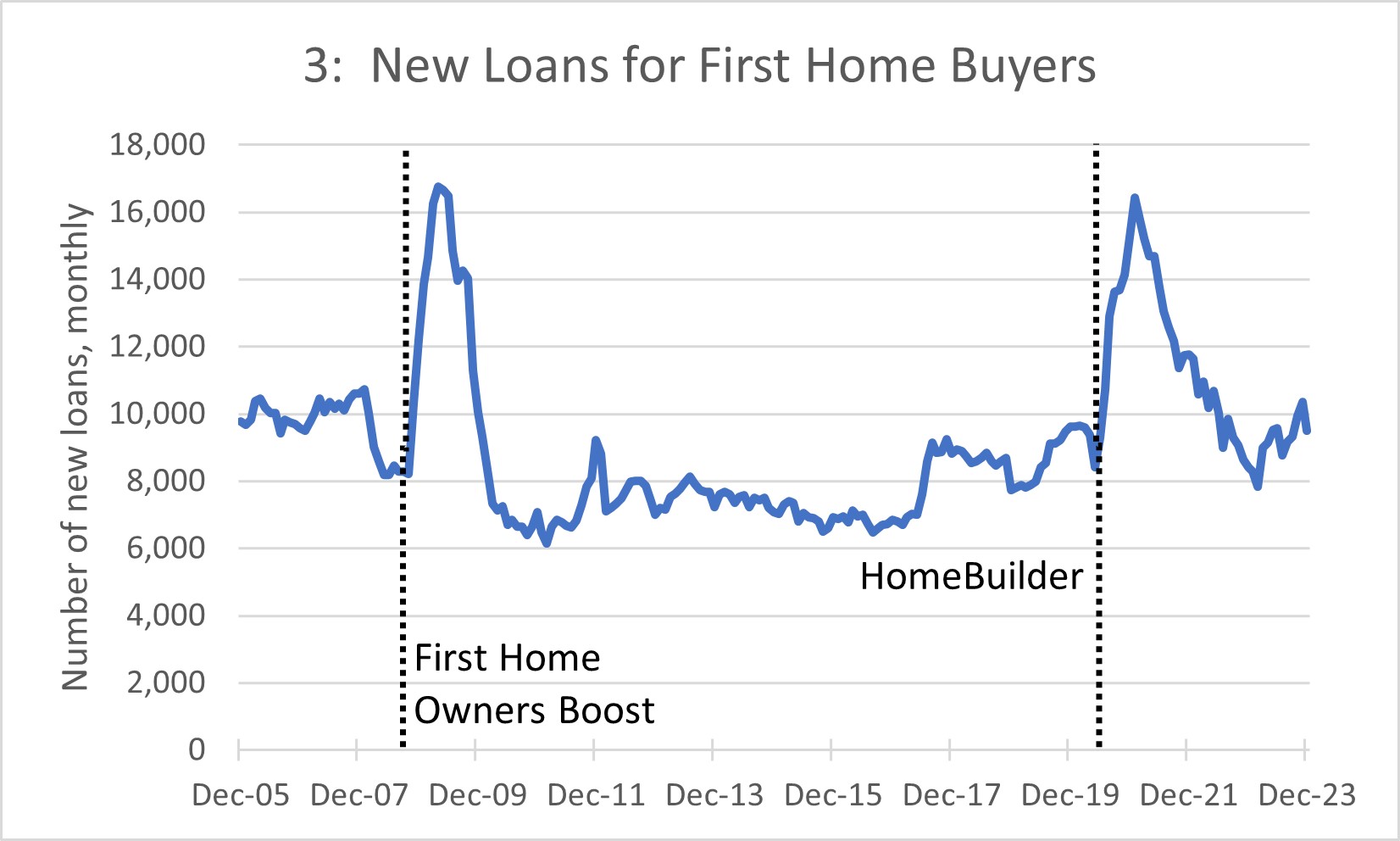

First homeowners react quickly and strongly to new finance. As shown in Chart 3, loans to owner-occupier first homeowners approximately doubled after the First Home Owners Boost of up to $14,000 in October 2008 and again after the HomeBuilder grants of up to $25,000 in June 2020.

Source: ABS Lending Indicators

This experience suggests that first home buying might also surge in response to availability of funds from superannuation. However, differences between the programs make quantifying that effect difficult. The programs above were subsidies, whereas accessing superannuation does not raise lifetime income and may even reduce it. Moreover, the increased grants were accompanied by other measures that boosted construction, in particular large reductions in mortgage rates.

The boost to saving and hence retirement security that might accompany increased home ownership is unclear. Historically, paying off a mortgage and building home equity has been a leading vehicle for saving for retirement. However, much of the wealth of current homeowners comprises capital gains, which may not be repeated. Moreover, a substantial share represents forced saving — in the sense that renters, unconstrained by commitments to repay principle, choose not to save as much. Whether this extra forced saving (on top of compulsory super) should be regarded as a cost or a benefit is unclear. Home ownership is financially advantageous for those enabled to avoid the old-age pension means test. From a social perspective, that is offset by an equivalent increased burden on taxpayers.

The more important benefits of home ownership may be non-financial, such as security of tenure and freedom to renovate.

The scenario and assumptions above are just one possibility, though it might be considered a central case. Another illustrative alternative is to assume that, instead of the first home buyer remaining in their home for the average 10 years, they were to remain there until retirement, so the loan is not repaid. This would represent a genuine “withdrawal” of superannuation.

Considering the example above, but extending the period of the loan from 10 to 30 years, and excluding repayment, the superannuation fund would be $58,427 lower at age 60-64. That compares with a median superannuation balance for 60–64-year-olds of $183,524 (Table 2). Lower superannuation balances would be partially offset by greater home equity.

The important point to make about large withdrawals like this is that they would be rare. Only 25% of home buyers remain in the one property for at least 20 years and only 5% for at least 40 years ((Bloxham, McGregor and Rankin 2010, Graph 3). So substantial withdrawals — that is, loans that are not repaid — from superannuation would be quite rare. That said, this scenario would be more relevant if the policy were modified so that loans could be rolled over to second and later home purchases.

The Coalition’s proposed Super Home Buyer Scheme resembles the Government’s Help to Buy Scheme. Both provide assistance with the deposit, repayable as a share of the capital gain. The fundamental difference is that under the Coalition’s scheme, the buyer is borrowing from their own superannuation, whereas under the Government’s scheme they borrow, at a concessional rate, from the taxpayer. Under the Coalition’s scheme, the buyer forgoes the earnings they would otherwise receive on their superannuation, whereas the Government’s scheme is a subsidy.3 Flowing from this, the Coalition scheme offers a moderate amount of assistance to a large number of home buyers, whereas the Government scheme provides large assistance to few buyers. Whereas the Coalition proposal is targeted at the 180,000 first home buyers a year (though not all these would be eligible), the Government’s proposal is restricted (via income and property value thresholds) to 40,000 borrowers. Whereas the Coalition is offering up to 40% of the superannuation balance (which might be $16,000 for a typical borrower), the Government is offering up to 40 per cent of the value of new homes and 30 per cent for existing homes.

The reduction in superannuation balances (by $10,734 in the central case discussed above) is a critical feature of the Coalition’s plan. Among some of the plan’s supporters, a diminution of the role of compulsory superannuation is a major advantage. However, the plan’s designers seem to have seen this as a problem, or at least as a complication – presumably this is why loans are limited to 40% of the balance or $50,000.

The reduction in retirement saving could be reduced if the loan had a higher interest rate. For example, in the United States, individuals can borrow from their retirement fund, called a 401k. Loans typically have a short repayment period and an interest rate tied to a benchmark like the prime rate, currently around 10% a year. A loan like that makes paying the deposit easier but subsequent loan repayments are harder.

Using Superannuation as Security

An alternative approach is to allow superannuation to be used as collateral for housing loans. This was proposed by the Falinski Report (see Sections 5.36 to 5.41 of ‘The Australian Dream: Inquiry Into Housing Affordability and Supply in Australia’).4

The idea is that deposits would decline by the full amount of the superannuation balance (or possibly more, if growth in the balance is expected). The size of the loan, and hence repayments, would increase commensurately. Superannuation balances would only be reduced in the infrequent and unexpected event of loan foreclosure. Legislation governing superannuation would need to be amended.

Because balances are unlikely to be touched, there is no clear reason for limiting the scheme. That applies both to limits on the proportion of the balance (as recommended in the previous section) or to limits on eligible recipients. The Falinski Report recommended that use as collateral be limited to first homeowners, but the reason for this is not apparent.

To be precise, Bergmann (2020) examined 2.8 million residential mortgages that were reported in the RBA’s Securitisation Dataset at any point between July 2015 and June 2019. Around 45,000 of these loans entered 90+ day arrears at some point during this period (around 1.5 per cent of loans) and only 3,000 loans (0.1 per cent) proceeded to foreclosure. There are reasons for suspecting this foreclosure rate to be unusually low. In particular, the period was short and saw rising house prices, though it also saw an increase in unemployment. But even if defaults were an order of magnitude greater, they might still be considered infrequent. The securitisation dataset is confidential; an update would require a request to the RBA.

Using superannuation as collateral has much in common with the previous policy of borrowing from superannuation, including the underlying rationale. In political terms, both policies transform superannuation from an obstacle to home ownership into a vehicle towards it. However, there are also differences, as summarised in the following table. For simplicity, it is assumed that the alternative to both policies is that the buyer saves for a larger deposit.

Table 3: Policy Comparisons

| Effect on: | Borrowing from super | Superannuation as collateral | ||

| Deposit | Reduced by 40% of super balance | Reduced by 100% of super balance | ||

| Mortgage payments | Unaffected | Higher | ||

| Homeowner’s capital gain | Lower | Unaffected | ||

| Superannuation balance | Lower | Normally unaffected | ||

Preferences between the two policies partly depend on how one weights the different rows. If protecting superannuation balances was most important (due to either economic considerations or political constraints), or if one thought that the deposit was the biggest hurdle to home ownership, collateral would be preferred. Alternatively, if one thought the biggest obstacle to ownership was high mortgage payments, borrowing from superannuation would be more effective.

Superannuation for Mortgage Offset Accounts

Senator Andrew Bragg has suggested homeowners be able to transfer their superannuation to their mortgage offset account.

So instead of earning the usual 4.5% real after-tax average return on superannuation, discussed above, the homeowner would save on mortgage payments. The RBA (Housing Lending Rates; Table F6) estimates that the average variable interest rate paid by owner-occupiers on outstanding loans in December 2023 was 6.4%. Adjusting for expected inflation of 2.6% (from indexed 10-year bond yields), that implies a real mortgage rate of 3.8%.

On average, homeowners would expect a lower average return from placing their assets in their mortgage offset account than in the average superannuation account. However, the offset account return would be more stable, predictable and liquid. And it would help to evade the old-age assets test.

The proposals in the previous two sections were aimed at assisting first home buyers, especially those encountering difficulties assembling a deposit. In contrast, use of offset accounts is aimed at providing relief for those who bought several years ago and are having difficulty making payments at much higher interest rates than they anticipated. Senator Bragg suggests a representative example might be a person in their 40s with a $1 million mortgage and about $150,000 to $200,000 in their superannuation account.

There is a strong case for allowing withdrawals from superannuation in periods of financial difficulty. However, homeowners are not obviously a top priority. People who lose their job or other source of income, recent family separations, people with large medical bills and other hardship cases might seem to have stronger claims. Especially as current homeowners, as of 2024, are likely to have enjoyed large capital gains. Indeed, in Senator Bragg’s example above, the homeowner is likely to have more home equity than they have in superannuation. A homeowner that has been making repayments over an extended period and has accumulated substantial equity will typically be able to refinance their mortgage.

Superannuation already allows for ‘hardship’ withdrawals. In practice, the hurdles to accessing these provisions are high and they are rarely used. There is a case for substantially increasing this access, especially as superannuation contributions increase. At higher contribution rates, the need for extra retirement saving diminishes and other worthwhile purposes for saving increase in relative importance. The argument that people make insufficient provision for their retirement applies to saving for other purposes also.

However, this is a broader issue of superannuation policy that has little to do with housing.

That said, high unexpected mortgage payments represent an important social and economic problem. Governments should be actively considering ways to ameliorate this shock and make it less likely to recur in future. At the top of this agenda should be removing distortions and obstacles to private sector remedies. In particular, homeowners would have more stable and predictable repayments if fixing mortgage rates was more common.

An important and unnecessary obstacle to fixed rate mortgages is APRA’s mortgage buffer. Lenders are required to assess borrowers’ capacity to repay a mortgage at an interest rate 3 percentage points higher than the contracted rate. This is to cover the contingency that the mortgage rate might rise. However, that contingency does not apply to fixed rate loans! By definition, there is no danger a fixed rate loan will change. Of course, rates fixed only for short horizons closely resemble variable rate loans.

A more sensible policy would pro-rata the buffer in relation to the proportion of a mortgage that is fixed for a substantial length of time, say, 5 years.5 With such a lower buffer, borrowers would be able to borrow more at fixed rates than at the variable rate.

Because fixed rate loans have less risk of default than variable rate loans, they should have a lower risk weight and incur lower capital requirements.

If APRA were to lower the capital requirements and reduce the buffer on fixed rate loans, more borrowers would take them out. The financial stresses created by the dramatic surge in mortgage rates over the past few years would be less likely to be repeated.

- Appendix: Sources and calculations for Section 5

| Row | Source / Formula | ||||||||

| (1) | Median superannuation balance 30-34 | $39,000 | ATO Tax Statistics reproduced on Table 2 | ||||||

| (2) | Borrowing limit | 40% | Liberal Party | ||||||

| (3) | Borrowed amount | $15,600 | = (1)x(2) | ||||||

| (4) | Average Real Capital Appreciation Rate | 2.4% | Fox and Tulip, 2014 | ||||||

| (5) | Median housing tenure (years) | 10 | Bloxham, McGregor and Rankin 2010 | ||||||

| (6) | Amount given back to Super Account | $19,775 | = (3)x(1+(4))^(5) | ||||||

| (7) | Superannuation rate of return | 4.5% | ASFA, Retirement Income Review | ||||||

| (8) | Lower balance at 40-44 | $24,226 | = (3)x(1+(7))^(5) | ||||||

| (9) | Difference after 10 years | $4,451 | = (8)-(6) | ||||||

| (10) | Value after a further 20 years | $10,734 | = (9)*(1+(7))^20 | ||||||

| (11) | Lower balance at 60-64 | $58,427 | = (3)x(1+(7))^30 | ||||||

All estimates are in constant 2024 dollars